Having $1 million is a huge advantage. Most people never reach this amount in their lifetime. But having the money is only half the battle. The real question is what you do with it.

You could put it in a savings account and earn almost nothing. Or you could make it work for you. The difference between these two choices is enormous. One family might earn $15,000 per year from their million dollars. Another family might earn $60,000 or more from the exact same amount.

The gap exists because of passive income. This is money you earn without working for it every single day. Your money makes money while you sleep, travel, or spend time with family. This is the dream many people talk about. The good news is that you can actually achieve it.

This article will show you exactly how to invest $1 million for passive income. You will learn about real options, not fake promises. Some strategies are safer than others. Some require more work than others. By the end, you will understand which approach fits your situation best.

What Is Passive Income and Why It Matters

Passive income is money that flows into your bank account without your active effort. You are not trading your time for payment. Instead, your money is working for you.

Think about it this way. When you work a job, you exchange time for money. You work 40 hours a week, you get paid. Stop working, and the paychecks stop. This is active income. Most people rely on this type of income. The problem is that you only have so many hours in a week.

Passive income is different. You do work upfront to set something up. Then, that investment generates income for months or years. The beauty is that you can earn from multiple sources at once. You might earn from dividend stocks, rental properties, and bonds all at the same time. Your total income can actually exceed what you could earn with a single job.

With $1 million, you have enough to create real passive income. A conservative approach might generate $20,000 to $40,000 per year. A more aggressive strategy might generate $50,000 to $80,000 annually. The exact amount depends on your choices and market conditions.

Why does this matter? Passive income provides security. It gives you choices. You might reduce work hours. You might retire earlier. You might take time off without stress. Financial freedom becomes possible instead of just a dream.

The Power of Diversification

Before you invest your million dollars, understand one important principle. Do not put all your money in one place. This is called diversification. It is the most important rule in investing.

Imagine you put $1 million into one stock. That company hits problems. The stock crashes 50 percent. You just lost $500,000. That is a painful lesson. Now imagine that same $1 million spread across 20 different stocks, bonds, real estate, and other assets. One investment drops 50 percent. You only lose about $50,000. Your other investments continue producing income.

Diversification also means mixing different types of investments. You might own stocks that pay dividends. You might own rental properties. You might own bonds. You might own index funds. Each type performs differently in different economic conditions. When one type struggles, another often thrives. This balance protects your income.

The goal is to create a portfolio that works in different situations. During good economic times, growth investments perform well. During slowdowns, stable income investments keep money flowing to you. You are not trying to get rich quick. You are building a reliable income machine.

Most financial experts recommend spreading your $1 million across several categories. A common approach divides money between stocks, bonds, real estate, and cash. The exact percentages depend on your age, goals, and comfort level. Younger investors might take more risk. Older investors typically want more safety.

Dividend Stocks as Your Foundation

Dividend stocks are one of the easiest ways to earn passive income. Here is how they work. You buy shares of a company. The company makes profits. Instead of keeping all the profits, the company pays some back to shareholders. This payment is called a dividend.

You earn money in two ways. First, the stock price might go up. Second, you collect dividends regularly. Many good dividend stocks pay quarterly. That means four payments per year. Some pay monthly. A few pay annually.

What makes a good dividend stock? Look for companies that have paid dividends for many years. Companies that increase their dividends over time are even better. These are usually large, stable businesses. They might be utility companies, banks, or established manufacturers. They are not flashy or exciting. They are boring. And boring is exactly what you want with passive income.

The dividend yield tells you how much income you will earn. If a stock costs $100 and pays $3 in annual dividends, the yield is 3 percent. With $1 million in dividend stocks yielding 3 percent, you would earn $30,000 per year. That is real money that shows up in your bank account.

A solid approach is to invest $300,000 to $400,000 in dividend stocks. Choose a mix of 15 to 25 different companies. You want different industries represented. You want different sizes of companies. You want a mix of dividend payment frequencies. This spread protects you if one company cuts its dividend.

Many investors use dividend exchange traded funds instead of picking individual stocks. These are like baskets that hold many dividend stocks. You buy one fund, and you own pieces of dozens of companies. This is simpler for most people. It requires less research and less monitoring.

Index Funds for Steady Growth and Income

Index funds are funds that track a market index. The most famous index is the S&P 500. This index includes 500 large American companies. An index fund that tracks the S&P 500 owns pieces of all 500 companies. You buy one fund, and you own a piece of the entire group.

Why are index funds perfect for passive income? First, they are incredibly simple. You do not need to pick individual companies. The index does that for you. Second, they are cheap. You pay very small fees. Third, they have historically done well over long periods. Since 1950, the S&P 500 has returned about 10 percent per year on average.

Index funds pay dividends too. The companies in the index pay dividends. The fund collects these and distributes them to you. Your dividend might be 2 percent per year. Combined with stock price appreciation, you might see 10 percent total growth per year. Much of that growth can be taken as income if you choose.

A smart strategy is to invest $300,000 to $400,000 in a mix of index funds. You might put half in US based index funds. You might put half in international index funds. This gives you exposure to companies around the world. It also provides diversification. When American stocks struggle, international stocks might do well.

The beauty of index funds is that they require almost no work. You buy them once. They automatically collect dividends. You do not need to research companies or watch news constantly. Most investors should own index funds as a core holding.

Real Estate Investment for Consistent Income

Real estate has created more millionaires than any other investment. A $1 million portfolio can include real estate in multiple ways.

The most straightforward approach is buying rental properties. You purchase a property, rent it out, and collect payments. The rent should exceed your mortgage, taxes, insurance, and maintenance costs. The difference is your profit. This happens every month. Over time, the tenant pays down your mortgage. Eventually, you own the property free and clear. At that point, almost all the rent is profit.

With $1 million, you might buy two or three rental properties using financing. Put 25 percent down on each property. That gives you $250,000 to $300,000 in down payments. Mortgages cover the rest. Now your money controls properties worth $1 million to $1.2 million. The tenants pay the mortgage. You pocket the difference between rent and expenses.

Real estate income is usually $8,000 to $15,000 per property per year after expenses. With two or three properties, you might earn $20,000 to $45,000 annually. This varies based on location, property condition, and tenant quality.

Another real estate approach is investing in Real Estate Investment Trusts, called REITs. These are companies that own real estate. They collect rent and distribute most of the income to shareholders. You can buy REIT stocks just like regular stocks. Many pay dividends of 4 to 6 percent. You get real estate income without managing tenants or dealing with repairs.

You might allocate $200,000 to $300,000 of your million to real estate. This could be down payments on rental properties or REIT purchases. Real estate is less liquid than stocks. You cannot sell it quickly. But it often provides higher income and tax advantages.

Bonds for Safety and Steady Income

Bonds are loans you give to companies or governments. In return, they pay you interest. Bonds are the safest type of investment. Your money is legally promised to be returned.

Government bonds are the safest. The US government has never defaulted on bonds. Corporate bonds are slightly riskier but still very safe. High quality corporate bonds have default rates under 1 percent.

Bonds pay interest regularly, usually twice per year. If you own a bond paying 5 percent, you get $50 per year for every $1,000 invested. With $200,000 in bonds at 5 percent yield, you would earn $10,000 per year.

Why would you want bonds if stocks pay more? Two reasons. First, bonds are safer. You do not wake up and find your bond worth half what it was yesterday. Your income is guaranteed. Second, bonds protect you in downturns. When stock markets crash, bond prices often rise. Your portfolio stays more stable.

Bond yields change based on interest rates. When the Federal Reserve raises rates, new bonds pay higher interest. Existing bonds pay less attractive interest, so their prices fall. When rates drop, new bonds pay less, but existing bonds become valuable. Rates are unpredictable. You cannot time them perfectly. But over long periods, bonds provide steady income.

You might keep $200,000 to $300,000 in bonds. Choose a mix of short term and long term bonds. Short term bonds are less risky if rates change. Long term bonds usually pay higher interest. A mix of both gives you stability and income.

Creating Your $1 Million Investment Plan

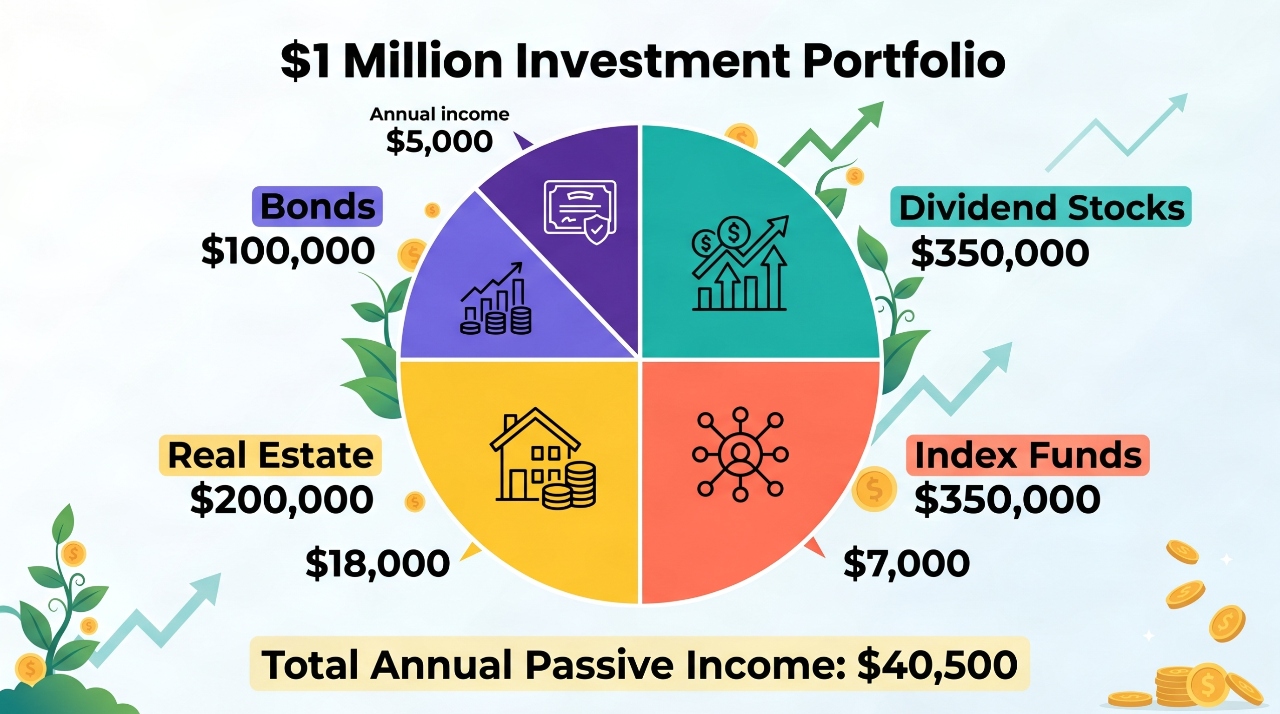

Now that you understand the options, let us create a sample portfolio. This is not advice for your specific situation. It is an example of how diversification works.

Investment Type: Dividend Stocks

Amount: $350,000

Expected Annual Income: $10,500 at 3% yield

Investment Type: Index Funds

Amount: $350,000

Expected Annual Income: $7,000 at 2% dividend yield

Investment Type: Real Estate

Amount: $200,000

Expected Annual Income: $18,000 from rental properties or REITs

Investment Type: Bonds

Amount: $100,000

Expected Annual Income: $5,000 at 5% yield

Total Investment: $1,000,000

Total Expected Annual Income: $40,500

This portfolio generates over $40,000 in passive income. It includes four different types of investments. If one performs poorly, the others continue producing income. This is the power of diversification.

The exact percentages matter less than the principle. You need diversity. You need a mix of safety and growth. You need investments that produce income regularly. Adjust the amounts based on your goals, age, and risk tolerance. Younger people might take more stock risk. Older people might want more bonds and real estate.

Where to Actually Invest Your Money

You need accounts to hold these investments. The main types are taxable brokerage accounts and retirement accounts.

Taxable brokerage accounts let you invest any amount. You can withdraw money anytime. You pay taxes on dividends and gains each year. Examples include accounts with Vanguard, Fidelity, or Charles Schwab. These accounts are flexible. They are perfect for most people with $1 million to invest.

Retirement accounts like 401k plans and IRAs have limits on how much you can contribute annually. You cannot withdraw money before retirement age without penalties. But you do not pay annual taxes on dividends or gains. Your money grows tax free. Once you reach retirement age, you can withdraw money. These accounts have major tax advantages for long term investing.

Many people use both types. Max out your retirement accounts first because of the tax benefits. Put the rest in taxable accounts. With $1 million, you will have plenty for both.

Opening an account is simple. Visit the website of a major brokerage. Complete an application. Deposit your money. You can start buying investments immediately. The whole process takes 15 to 30 minutes.

Do not stress about timing the market. You do not have to invest all $1 million on the same day. You can invest it gradually over weeks or months. This is called dollar cost averaging. You reduce the risk of investing everything at a market peak. It also gives you time to get comfortable with each investment.

How Much Income Can You Actually Expect

Your actual income depends on three things. First, what types of investments you choose. Second, how much you are willing to take as income. Third, market conditions.

Most portfolios will naturally generate 2 to 4 percent per year in dividends and interest. With $1 million, that is $20,000 to $40,000 annually. This is very conservative. Your money also appreciates in value. Historically, diversified portfolios grow about 7 to 8 percent per year on average.

You could take all the dividends and interest as income. You could also reinvest some gains and take only part as income. If you take less than your total returns, your portfolio grows. This is smart because inflation eats away at your purchasing power. If you take your full returns, your portfolio stays roughly the same size.

For example, imagine your portfolio generates $40,000 in income and appreciates $30,000 in value. You have $70,000 in total returns. You could take $40,000 as income and let the appreciation reinvest. Your portfolio stays at $1 million. You earn $40,000 per year forever, assuming returns stay consistent.

Or you could take $50,000 per year. Your portfolio shrinks slightly. But you still have good income. This approach might work if you want to live off your investments.

Be realistic about market conditions. Some years will be great. Returns might be 15 or 20 percent. Other years will be terrible. Markets might drop 30 or 40 percent. Your income might drop too. Over long periods, returns average out. But individual years are unpredictable.

Taxes and How to Minimize Them

Taxes eat into your income. Understanding taxes helps you keep more money.

Dividend income is taxed. The tax rate depends on the type of dividend and your income level. Qualified dividends usually get taxed at lower rates than ordinary income. In the US, qualified dividends might be taxed at 0, 15, or 20 percent depending on your income. Ordinary dividends use your regular tax rate, which might be 22, 24, or higher.

Interest income from bonds is taxed as ordinary income. This is at your regular tax rate. If you are in the 24 percent tax bracket, you pay 24 cents in taxes for every dollar of bond interest.

Real estate has different tax treatment. Rental income is taxed. But you can deduct expenses like mortgage interest, property taxes, insurance, and repairs. These deductions often reduce your taxable real estate income significantly. This makes real estate tax efficient.

Capital gains are profits from selling investments for more than you paid. These are taxed when you sell. If you bought a stock for $100 and sold for $150, the $50 gain is taxable. Long term capital gains (held over one year) are taxed at lower rates than short term gains.

Tax advantaged accounts like 401k plans and IRAs reduce taxes. You do not pay taxes on dividends or gains inside these accounts annually. You only pay taxes when you withdraw money. This lets your money grow faster inside these accounts.

To minimize taxes, max out retirement accounts first. Use tax efficient investments like index funds in taxable accounts. Hold investments long term to get capital gains rates. Consider municipal bonds if you are in a high tax bracket. They often pay tax free interest.

Managing Your Investments Over Time

Investing is not a set it and forget it activity. You need to check on your portfolio occasionally.

Every year, review your allocations. If stocks have done well, they might be 60 percent of your portfolio instead of 50 percent. You can rebalance by selling some stocks and buying bonds or real estate. This keeps your portfolio aligned with your plan.

Rebalancing actually helps you buy low and sell high. When you rebalance, you are selling investments that have done well and buying investments that have lagged. This is the opposite of most people’s instincts. Most people want to buy winners. Smart investors buy the laggards.

Check on your dividend and interest payments. Make sure you are receiving what you expect. If a dividend drops unexpectedly, investigate why. Sometimes this is fine. Sometimes it signals a problem. Look at your rental properties once a quarter. Make sure rent is being paid and properties are maintained. Check your bond interest payments. Make sure they arrive on schedule.

Do not panic during market downturns. Stock markets drop regularly. This is normal. Your bonds and real estate income continue flowing in. Your dividend stocks might drop in price, but most still pay their dividends. Do not sell everything during a crash. This locks in losses. Historically, markets always recover.

Rebalance once or twice per year. Do not trade constantly. Do not check prices daily. Long term investing requires patience. You are building income, not trying to get rich quick.

Common Mistakes to Avoid

Many people make mistakes with $1 million that destroys their passive income plans.

Mistake One: Putting all money in one investment. You learned about diversification already. This cannot be overstated. One bad investment can wipe out huge gains. Spread your money across different types of investments.

Mistake Two: Chasing high returns. Some investments promise 10, 15, or even 20 percent returns. These are usually risky or fraudulent. Sustainable passive income comes from real companies, property, and bonds. These provide 4 to 8 percent returns realistically. Do not risk your principal for slightly higher income.

Mistake Three: Not having an emergency fund. Invest $1 million for passive income, but keep some cash separate. You should have $15,000 to $30,000 available for emergencies. This prevents you from selling investments at bad times. When your car breaks down or you need a medical procedure, you use your emergency fund, not your investments.

Mistake Four: Ignoring taxes. Taxes reduce your income significantly. Many new investors forget this. Plan your investments with taxes in mind. Use tax advantaged accounts. Consider tax consequences before buying and selling. This keeps more money in your pocket.

Mistake Five: Trying to time the market. Most professionals cannot predict market movements consistently. You certainly cannot either. Do not wait for the perfect moment to invest. Invest gradually or invest all at once. Both work fine over long periods. The best time to invest is when you have money to invest.

Starting Your Passive Income Journey

You now understand how to invest $1 million for passive income. The concepts are not complicated. Diversify across stocks, bonds, real estate, and cash. Choose stable investments that produce income. Hold them long term. Rebalance occasionally. Ignore short term noise.

Starting is the hardest part. You might feel overwhelmed. You might wonder if you are making the right choices. This is normal. Remember that perfection is not required. A good plan executed immediately beats a perfect plan delayed indefinitely.

Begin by opening accounts with a major brokerage. Choose between Vanguard, Fidelity, or Charles Schwab. They all work well. The differences are minor. You might open a regular brokerage account and a retirement account.

Next, research specific investments. Look at dividend stocks that have paid steadily for 10 plus years. Look at index funds that track major indexes. Look at real estate opportunities in your area or REIT funds. Look at bond funds. Make a list of specific investments you want to own.

Then, start buying. You do not need to buy everything at once. Start with index funds. They are simple and effective. As you get comfortable, add dividend stocks. Add bonds. Add real estate. Build your portfolio gradually.

You might buy $100,000 in month one. Another $100,000 in month two. Continue until your million dollars is fully invested. This approach is less overwhelming than doing everything at once. It also reduces risk from buying everything at market peaks.

Finally, set up a system to track your income. Create a simple spreadsheet. Record your dividend payments, interest payments, and rental income. Add these up annually. You will be amazed by the money flowing in without active work.

Adjusting Your Plan as Life Changes

Your $1 million investment plan is not permanent. Life changes. Your needs change. Your plan should adjust accordingly.

If you get older, you might want less stock risk. You could shift money from stocks to bonds. Your income might be more stable. It might not grow as fast, but stability matters more as you age.

If you face an unexpected expense, you can withdraw from your taxable accounts. This is one advantage of taxable accounts over retirement accounts. You can access the money without penalties.

If your income needs change, you can adjust what you are taking from your portfolio. Maybe you need more income next year. You could sell some growth investments that have appreciated significantly. Or you could take more from your bonds and dividends.

If you inherit more money or sell a business, you can invest additional amounts. Your portfolio might grow to $2 million or $3 million. Adjust your allocations accordingly. The principles remain the same. Diversify. Keep costs low. Focus on income producing assets.

The Long Term Vision

With $1 million wisely invested for passive income, you are not just earning money. You are building financial freedom. You are creating options that most people never have.

In year one, your portfolio generates $30,000 to $50,000 in passive income. This is real money. In year five, your portfolio has likely grown. You might earn $40,000 to $60,000 annually. In year ten, you might be earning $50,000 to $70,000 or more. This assumes you reinvest some gains and market returns are decent.

This income compounds. It grows on itself. Money you earn from dividends can be reinvested to earn more dividends. This creates exponential growth over decades.

Eventually, your passive income might exceed your needs. You have complete financial freedom. You work because you want to, not because you have to. You can retire at 50 or even 40. You can take career risks. You can pursue dreams. This is possible because of passive income.

Conclusion

Investing $1 million for passive income is the smartest decision you can make with significant money. You have learned the concepts, strategies, and specific steps.

Start with diversification across stocks, bonds, real estate, and cash. Build your portfolio with dividend stocks, index funds, REITs, bonds, and perhaps rental properties. Open accounts with a major brokerage. Buy stable investments gradually. Rebalance annually. Ignore short term market noise.

Your first year income might be $30,000 to $50,000. This is meaningful money. Over time, your portfolio grows. Your income grows. You build financial freedom.

Do not wait for the perfect moment or the perfect investment. That moment never comes. Start today. Open an account. Buy your first investment. Build momentum. In five years, you will be amazed by the passive income flowing into your account every month.

Your financial future is not determined by luck or outside factors. It is determined by your decisions today. Decide to invest your $1 million wisely. Decide to build passive income. Decide to take control of your financial future. Then execute your plan with patience and discipline.

The best time to start was yesterday. The second best time is today.