About 60 percent of Americans have less than $1,000 in savings. That’s a stunning number. If you have $100,000 to invest, you’re already ahead of most people. The real question isn’t whether you can invest this money. It’s how you can make it work for you without doing much work at all.

Passive income means money that comes in regularly without you having to trade your time for it. With $100,000, you can build multiple streams of passive income. Some methods take a few months to start working. Others take a couple of years. But all of them can help you reach financial freedom faster.

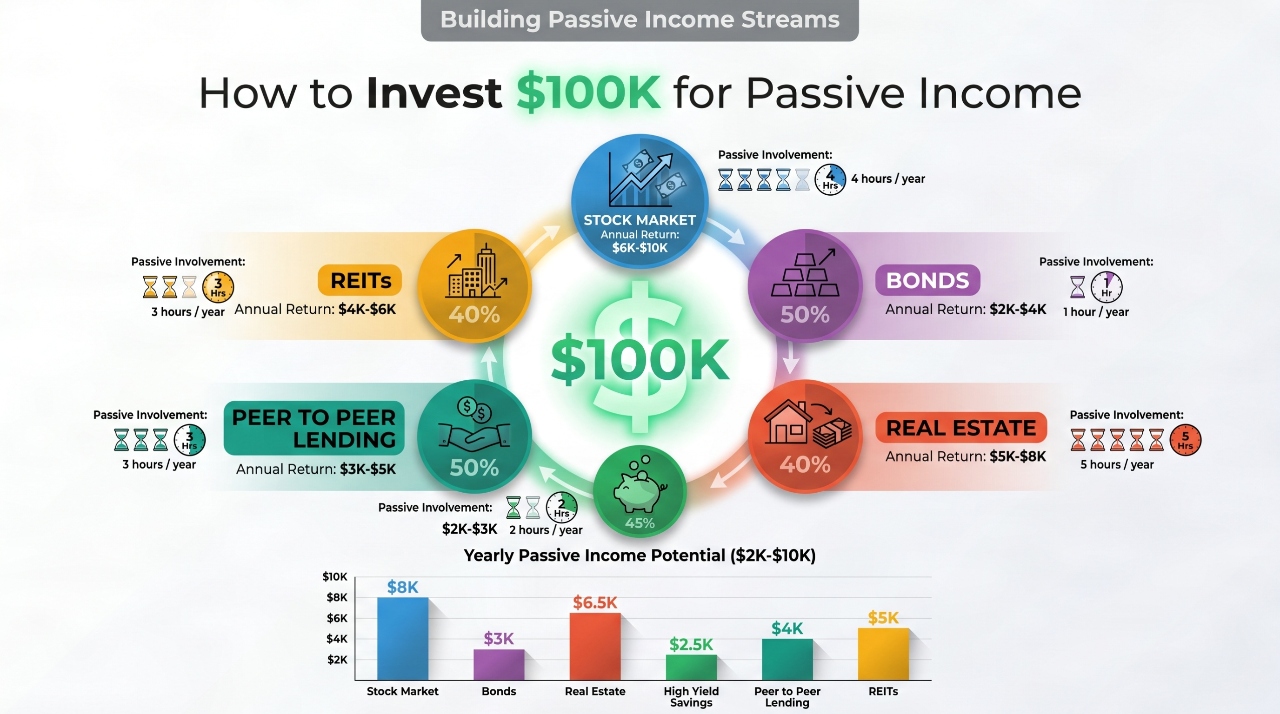

This guide shows you real ways to invest $100,000 for passive income. We’ll skip the hype and focus on strategies that work. You’ll learn what fits your situation, how much money each method needs, and what returns you might expect.

Why Passive Income Matters More Than You Think

Most people trade time for money. You work 40 hours a week to get a paycheck. That works fine until you can’t work anymore. Passive income is different. You set things up once, and money comes in while you sleep, travel, or spend time with family.

Having passive income gives you options. You can leave a bad job. You can take care of a sick family member. You can retire early if you want to. With $100,000, you could generate anywhere from $3,000 to $10,000 per year in passive income, depending on what you choose.

The best part? You don’t need to be rich or lucky to do this. You just need a plan and the willingness to stick with it.

The Stock Market: Start Simple With Dividends

The easiest way to invest $100,000 is through the stock market. You don’t need to pick individual stocks or watch the market constantly. Instead, you can buy dividend stocks or index funds that pay you regularly.

What are dividends? When you own a piece of a company through stock ownership, that company sometimes pays you a portion of its profits. This payment is called a dividend. Some companies pay dividends every three months. The money hits your account automatically.

A dividend stock might give you between 2 and 5 percent per year. With $100,000, that means $2,000 to $5,000 yearly. It’s not huge money, but it’s real money for doing almost nothing.

Index funds make this even easier. An index fund holds hundreds or thousands of stocks in one fund. Instead of picking winners and losers, you own a little piece of the whole market. Funds like the S&P 500 index have an average dividend yield around 1.5 to 2 percent.

You can buy these through any brokerage account. Popular brokers include <a href=”https://www.fidelity.com”>Fidelity</a>, <a href=”https://www.vanguard.com”>Vanguard</a>, and Charles Schwab. The process takes about 20 minutes. You pick your fund, deposit your money, and you’re done.

One risk to remember: stock prices go up and down. Your $100,000 might become $95,000 or $110,000 depending on market conditions. But if you hold for years, history shows that stocks trend upward over time. Most dividend investors don’t panic about short term drops. They keep collecting their dividends and wait for prices to recover.

Bonds: The Safer Route for Steady Income

If stock market ups and downs keep you awake at night, bonds might be your answer. A bond is basically a loan you give to a company or government. They pay you back with interest.

Government bonds are the safest option. You buy a bond, and the government pays you interest regularly. The interest is predictable. Treasury bonds currently pay around 4 to 5 percent per year. That means $4,000 to $5,000 on $100,000. Your money is nearly guaranteed.

Corporate bonds pay higher interest because they’re slightly riskier. A solid company might pay 5 to 6 percent. Again, with $100,000, you’re looking at $5,000 to $6,000 yearly.

Bond funds bundle many bonds together, which spreads your risk. You can buy a bond fund just like you buy a stock fund through any brokerage. The income comes regularly, usually monthly or quarterly.

The downside of bonds is predictability works both ways. You know what you’ll make, but you won’t make more if investments go well. If interest rates rise, your existing bonds become less valuable if you need to sell them. But if you hold to maturity, you get your full investment back plus all your interest payments.

Many smart investors split their $100,000 between stocks and bonds. Maybe $60,000 in stocks for growth and $40,000 in bonds for stable income. This mix gives you both regular payments and growth potential.

Real Estate: Build Wealth Brick by Brick

Real estate is different from stocks and bonds. You can actually touch it. Real estate also creates passive income in two ways: rental income and property appreciation.

Rental properties are straightforward. You buy a property, rent it to tenants, and keep the difference between what they pay and your expenses. With $100,000, you could put a down payment on a rental property worth $300,000 to $400,000 depending on your area.

A rental property might cost you $1,500 monthly in mortgage, property taxes, insurance, and maintenance. If you rent it for $2,200, you pocket $700 per month or $8,400 yearly. This number improves over time as you pay down your mortgage and rents typically rise.

Real estate takes more work than stocks or bonds. You need to find a good property, manage tenants, handle repairs, and keep up with legal stuff. But the passive income is real, and your tenants help you pay down the mortgage.

Real estate crowdfunding offers a middle ground. Companies like <a href=”https://fundrise.com”>Fundrise</a> and <a href=”https://www.realtymogul.com”>RealtyMogul</a> let you invest in real estate projects without buying property yourself. You get income from the project, but a company handles the details.

Returns vary from 6 to 12 percent depending on the deal. With $100,000, you might make $6,000 to $12,000 yearly. The money is less passive than stocks because some projects fail. But many investors like spreading $100,000 across multiple crowdfunding projects instead of betting on one rental property.

High Yield Savings and CDs: Peace of Mind Money

Sometimes you want to keep things simple. High yield savings accounts and certificates of deposit offer that simplicity.

Banks keep interest rates low, but online banks offer higher rates. Currently, high yield savings accounts pay around 4 to 5 percent. That means $4,000 to $5,000 yearly on $100,000. Your money is totally safe, and you can access it whenever you need it.

A CD works similarly but you lock your money away for a set period like six months, one year, or five years. You can’t touch it without paying a penalty. In return, the bank pays you slightly more interest. You might get 4.5 to 5.5 percent on a five year CD.

The downside is that inflation eats into your returns. If inflation is 3 percent and you’re earning 5 percent, your real return is only 2 percent. But some passive income is better than no passive income.

Many investors use high yield savings or CDs for part of their $100,000. It provides stable income while they invest the rest in stocks or real estate.

Peer to Peer Lending: Higher Returns With More Risk

Peer to peer lending platforms connect people who want to borrow money with people who want to lend it. You become the lender.

When someone borrows $5,000 through the platform to pay off credit card debt, you might lend part of that money. You get back the principal plus interest. Popular platforms include Prosper and LendingClub.

Returns typically range from 5 to 8 percent, but some loans default. That means the borrower doesn’t pay you back. The platform spreads your $100,000 across hundreds of loans so one default doesn’t kill you. Even after some defaults, many investors average 5 to 6 percent returns.

This method requires some attention. You should review loan details before investing. Some investors use platforms to automate the process and let the system pick loans for them.

The risk is higher than stocks or bonds because these are regular people borrowing money. Your $100,000 isn’t insured like bank deposits are. But many investors accept this risk for higher returns.

Dividend Aristocrats: Companies That Keep Paying

Some companies have paid dividends for over 25 years straight. These are called dividend aristocrats. They’re stable, profitable businesses that treat shareholders well.

Companies like Johnson and Johnson, Coca-Cola, and Procter and Gamble are famous examples. They usually pay 2 to 3 percent dividends yearly. With $100,000 invested in these stocks, you’d get $2,000 to $3,000 yearly.

The benefit of dividend aristocrats is reliability. These aren’t flashy growth stocks. They’re boring companies that print money. You buy them, collect checks, and don’t think much about them.

You can buy individual dividend aristocrat stocks, or you can buy a fund that specializes in them. The fund approach is easier because professionals pick the stocks for you. Either way, you’re getting paid regularly by solid businesses.

REITs: Real Estate Without the Headaches

A REIT is a real estate investment trust. It’s essentially a company that owns real estate. When you buy REIT stock, you own a piece of that real estate.

REITs pay dividends regularly. Many pay 3 to 5 percent yields. With $100,000, that’s $3,000 to $5,000 yearly. You get real estate exposure without owning property, managing tenants, or dealing with repairs.

You buy REITs just like regular stocks through any brokerage. Popular REITs own shopping centers, apartments, warehouses, and office buildings. Some specialize in specific property types.

The advantage over owning rental property directly is liquidity. If you need your money, you can sell REIT shares immediately. Selling actual property takes months and costs thousands in fees.

The disadvantage is that you don’t control the property. Management decisions are made by other people. Also, REIT dividends are taxed as regular income instead of capital gains for most people, which means you might owe more taxes.

Many investors love REITs because they get real estate income without active management. You could split your $100,000 between REITs and other investments to reduce risk.

Creating a Balanced Portfolio That Works

You don’t have to pick just one method. In fact, you shouldn’t. Most successful passive income investors spread their money across multiple investments. This strategy is called diversification.

A simple approach for $100,000 might look like this: put $40,000 in dividend stock funds, $30,000 in bonds or bond funds, $20,000 in REITs, and $10,000 in high yield savings.

With this mix, you’d get roughly $2,800 in yearly passive income from dividends, $1,500 from bonds, $900 from REITs, and $500 from savings. That’s $5,700 total, or about 5.7 percent return.

Your actual returns would vary based on market conditions and which specific investments you pick. But this gives you a real target to aim for.

Different people have different risk tolerances. Someone near retirement might want more bonds and fewer stocks. A younger person with 30 years until retirement can afford more stocks and REITs. Your personal situation matters.

How Much Time This Actually Takes

One question people ask is how much time passive income really takes. The honest answer is it depends on your method.

Stock and bond funds take minimal time after setup. You invest, and income arrives automatically. Maybe you check your account quarterly. That’s it.

Rental properties take ongoing time. Tenants need to be managed, repairs come up, and you must stay on top of legal requirements. Plan on five to ten hours monthly for one property.

Dividend aristocrats and REITs are like stock funds in terms of time. You buy and monitor occasionally.

Peer to peer lending and crowdfunding take a bit more attention when you’re starting out. After setup, you might review performance monthly.

Most people can easily manage $100,000 across multiple passive income methods with just a few hours per month.

Tax Stuff You Should Know

Passive income is still income to the IRS. You have to pay taxes on it. The amount you pay depends on what type of investment generates the income.

Qualified dividends get special tax treatment. You might pay only 15 or 20 percent taxes instead of your regular income tax rate. That’s one reason dividend stocks are popular.

Bond interest is taxed as regular income. If you earn $2,000 in bond interest, you might owe taxes on it at your normal tax rate.

Real estate rental income is also taxed as regular income, but you can deduct expenses like mortgage interest, repairs, and property taxes.

Tax rules are complicated, so talk to a tax professional before investing. They can show you the best strategy for your situation.

Just because you have to pay taxes doesn’t mean passive income is bad. Even after taxes, most of these methods beat keeping money in a regular savings account earning 0.01 percent.

Common Mistakes to Avoid

Investing too much in one thing is a major mistake. People sometimes put all $100,000 in one stock, one property, or one investment. If that single investment fails, you lose everything. Spread your money across multiple investments.

Chasing high returns is another trap. Someone promises 15 percent returns guaranteed. That’s a red flag. Realistic returns are 4 to 8 percent for most passive income methods. Anything promising much more is risky or fake.

Giving up too soon happens more often than you’d think. Passive income takes time to build. Don’t expect huge cash flow in month one. Stick with your plan for at least three to five years.

Ignoring inflation eats away at your gains. If inflation runs 3 percent and your investments earn 4 percent, you’re only making 1 percent real money. Keep this in mind when planning.

Not having an emergency fund is dangerous. Never invest all your money. Keep three to six months of expenses in an emergency fund before investing $100,000.

Getting Started Right Now

Step one is opening a brokerage account. Fidelity, Vanguard, and Charles Schwab make this easy. It takes 15 minutes online. You’ll need your social security number and basic information.

Step two is deciding your allocation. How much stocks, bonds, real estate, and other investments do you want? Write this down.

Step three is buying your first investments. Start with one or two to keep things simple. You can add more later.

Step four is setting up automatic dividends. Most brokerages let you reinvest dividends automatically. Your money grows faster this way.

Step five is checking your progress quarterly. But don’t obsess. Passive income is supposed to be hands off.

The Bottom Line

You have $100,000. That’s real wealth that most people don’t have. With smart choices, you can turn that into $4,000 to $10,000 yearly in passive income. That money might not replace your job, but it gives you options and builds toward financial freedom.

The best investment is the one you’ll actually stick with. If real estate excites you, start there. If stocks feel comfortable, go that route. The method matters less than actually starting and staying consistent.

Your future self will thank you for the work you do today. Financial independence isn’t a fantasy. It’s something you build one decision at a time.

Take Action Today

You have everything you need to get started. Open a brokerage account this week. Pick one investment method. Put your $100,000 to work. In a few years, you’ll be collecting passive income regularly.

Don’t wait for the perfect moment. That moment is now. Your financial future depends on decisions you make today. Start investing and start building the passive income stream you deserve.