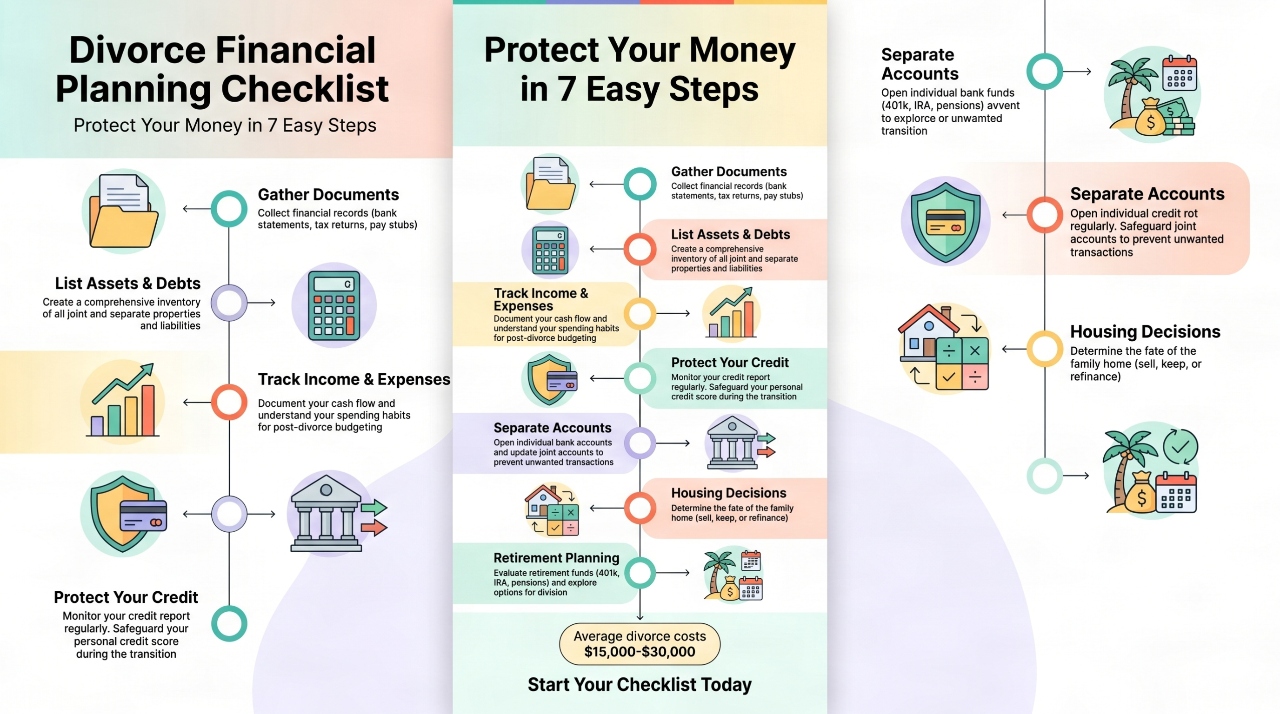

Divorce costs the average American between $15,000 and $30,000, according to recent data. That number climbs even higher when children are involved or when couples have complex financial situations. Money stress during divorce ranks among the top reasons people feel overwhelmed during this difficult time.

Here’s what many people don’t realize: the financial decisions you make today will affect your life for years. A single mistake with retirement accounts or property division could cost you thousands of dollars. The good news is that a simple checklist can help you avoid these mistakes and protect what matters most.

This guide gives you a practical plan. You won’t need special knowledge or experience to use it. Just follow the steps in order, and you’ll have a clear picture of your finances and know exactly what comes next.

Gather Your Financial Documents First

Before you do anything else, you need to know what you own and what you owe. This sounds basic, but most people skip this step, which creates huge problems later.

Start by collecting every financial document you can find. Look for bank statements from the past year. Find your investment accounts, retirement statements, and insurance policies. Locate your mortgage documents and any other loan paperwork. Check your files for credit card statements and utility bills.

Create a folder on your computer or a physical folder in your home. Put copies of everything in this folder. Scan documents if you want to be extra safe. Make sure you have access to online accounts and know all the passwords.

What specific documents you need:

Bank accounts including checking, savings, and money market accounts need recent statements. Investment accounts like brokerage accounts and trading accounts require current statements showing all holdings. Retirement accounts including 401(k)s, IRAs, pensions, and SEP IRAs must be documented with recent statements. Real estate property should have the deed and recent property tax assessments. Vehicles need titles and registration documents. Insurance policies including life, health, and homeowner’s insurance require current documents. Business interests, whether you own a part or all of a business, need documentation of value and ownership. Credit cards and lines of credit should have all statements from recent months.

Don’t get stressed if you can’t find everything right away. Your attorney or a financial professional can help you locate missing documents. The important thing is to start gathering what you have access to now.

List All Your Assets and Debts Honestly

Now that you have your documents, it’s time to make a complete list. This is one of the most important steps in your checklist because it affects everything that comes next.

Write down everything you own that has value. Include your house, car, jewelry, art, furniture, and electronics. Don’t leave anything off because you think it’s not important. Even small items add up when you have many of them.

Value everything as honestly as you can. If you’re not sure about something’s value, look it up online or ask a professional appraiser. Your house might need professional appraisal. Your jewelry might need evaluation by a jeweler. A business definitely needs a professional business valuation.

Now list everything you owe money on. Include your mortgage, car loans, credit card debt, medical bills, and personal loans. Add student loans even if you haven’t been paying them recently. Include any money you owe to family members or friends. Don’t forget taxes you might owe to the government.

The total of everything you owe is your total debt. Subtract that from your total assets. What’s left is your net worth. This number matters because it shows what you’re actually working with when dividing things in the divorce.

Understand Your Income and Monthly Expenses

Your income affects everything in a divorce. It determines child support, spousal support, and what you can afford to live on. You need to know exactly how much money comes in each month.

Gather all your income documentation. If you work for someone else, get your recent pay stubs and tax returns. If you’re self employed, collect your profit and loss statements. Include any rental income, investment income, or side income sources. Add any benefits you receive from the government or other sources.

Your monthly expenses are equally important. Pull out your credit card statements and bank statements from the last three months. Write down everything you spend money on including housing, food, transportation, insurance, medical care, childcare, and entertainment. Include subscriptions you might forget about like streaming services or gym memberships.

Be honest about your spending. Don’t estimate low because you think it looks better. You need accurate numbers to make good decisions. If your expenses seem high, you have another job ahead of you. You’ll need to figure out a realistic budget for after the divorce. This becomes critical when determining if you can afford to keep the house or if you need to downsize.

Protect Your Credit Before Things Get Worse

Your credit score affects how much you’ll pay for borrowing money for years after the divorce. Taking action now prevents serious damage.

First, check your credit report. You can get a free report from www.annualcreditreport.com once a year. Look through the entire report. Dispute any errors you find. Report any accounts you don’t recognize.

Next, monitor your accounts carefully. If you have joint credit cards, consider whether you need to close some of them. This is tricky because closing accounts can hurt your credit score. But leaving joint accounts open means your ex could rack up charges that affect you both. Work with your attorney on the best timing for this step.

Make all your payments on time from now on. One late payment can drop your score significantly. Set up automatic payments if that helps you remember. Payment history is the biggest factor in your credit score, so this one action matters more than almost anything else.

Consider getting your own credit card in your name alone if you don’t have one already. This helps you build a separate credit history from your ex. You don’t need to use it much. Just keep it open and active.

Separate Your Bank Accounts and Financial Accounts

Once you’ve gathered your documents and know what you have, it’s time to separate your finances. This protects both you and your ex from future problems.

If you have joint bank accounts, consider opening a new account in your name only. Don’t close the joint account without talking to your attorney first because that could cause legal problems. Instead, start moving your paycheck to your new account. You can keep the joint account open for shared expenses like the mortgage until the divorce is final.

Do the same with credit cards if possible. Get a new credit card in your name only. If you need to use a joint card, keep careful records of what you buy. Mark what’s for shared expenses and what’s for your personal use.

For investment accounts and retirement accounts, don’t touch them without professional advice. The rules for dividing these accounts are complicated and changing them without proper documents can create huge tax problems. This is one area where you absolutely should get help from a professional.

Get your own safe deposit box at a bank if you don’t have one. Store important documents there like property deeds, insurance policies, and your important financial information. Make sure your ex doesn’t have access to it.

Review Your Insurance Needs Carefully

Insurance protects your financial future. Changes during divorce often leave people underinsured or overinsured. You need to review everything.

Health insurance is the first priority. If you’re covered under your ex’s employer plan, you’ll lose that coverage after the divorce is final. Look into getting your own health insurance right away. You might qualify for coverage through your own job or through the government marketplace. Factor the cost into your divorce settlement negotiations.

Life insurance becomes important if you have children or if you’re planning to receive spousal support. Your ex might require you to maintain life insurance as part of the settlement agreement. Make sure you understand these requirements and budget for them.

Homeowner’s insurance is critical if you’re keeping the house. Review your policy to make sure the coverage is adequate. If you’re selling the house, you’ll still need renters insurance for whatever housing you move to next.

Auto insurance is required by law. Make sure your policy stays active and covers you adequately. Some people try to save money by dropping coverage during divorce, which is a mistake that can cost thousands if you’re in an accident.

Consider umbrella liability insurance if you have significant assets. This covers you if someone sues you for more than your other policies cover.

Child Support and Custody Financial Planning

If you have children, child support and custody arrangements affect your finances dramatically. You need a clear plan for how this will work.

Each state has different child support guidelines. The amount is usually based on both parents’ income and how much time each parent spends with the children. Your attorney can explain how your state calculates this number. The important thing is to budget for it carefully.

If you’ll be paying child support, make sure you understand the monthly amount and when payments are due. Build this into your monthly budget. If you’ll be receiving child support, don’t count on it as guaranteed income because sometimes the paying parent falls behind. It’s better to budget without it and treat it as extra money when it arrives.

Beyond child support, think about other child related expenses. Who pays for medical insurance? Who covers copays and deductibles? Who pays for dental work, glasses, or braces? Who covers school fees, sports equipment, and extracurricular activities? Getting these details in writing prevents endless arguments later.

Childcare costs are huge for many families. If you work and need childcare, factor this into your budget and your divorce settlement. Sometimes parents share these costs. Sometimes one parent covers them. Make sure you’re clear on the arrangement.

College expenses create another financial planning challenge. Some divorce settlements include agreements about college costs. Discuss this with your attorney early because it affects the overall settlement.

Plan Your Post Divorce Housing Situation

Housing is usually the single biggest expense in any household budget. Your housing decision during divorce affects your finances for years.

First, decide whether you want to keep the house or sell it. Keeping the house sounds good emotionally, but the math might not work. Calculate the mortgage payment, property taxes, insurance, maintenance, and utilities. Compare this to the cost of renting something similar. Many people find that selling and renting is more affordable than keeping a house they can’t afford alone.

If you’re selling the house, you’ll split the proceeds with your ex. Remember to account for real estate agent commission, which typically runs 5 to 6 percent of the sale price. You’ll also owe capital gains taxes if the house has gone up significantly in value since you bought it. Your tax professional can calculate this for you.

If you’re keeping the house, make sure the house transfer is documented properly. Get the deed changed to remove your ex’s name. Refinance the mortgage in your name only if needed. Make sure insurance is updated to show only you as the owner.

If you’re renting, start looking for a place you can afford based on your post divorce income. This helps you understand what lifestyle changes might be necessary. Renting gives you flexibility to move later if your financial situation changes.

Handle Retirement Accounts Properly

Retirement accounts represent some of the most valuable assets in a divorce. The rules for dividing them are strict, and mistakes can trigger massive tax bills.

If you’re dividing a 401(k) or similar employer plan, you need a legal document called a QDRO (Qualified Domestic Relations Order). This tells the plan administrator how to split the account. Without this document, you can’t touch the money without penalties and taxes. Your attorney should handle this.

For IRAs and other individual retirement accounts, the rules are simpler. Your ex gets added as a beneficiary or the account is split. Either way, this must be done correctly by the financial institution handling the account.

Social Security benefits are a special case. If you were married for at least ten years, you might be entitled to benefits based on your ex’s work history. You don’t divide Social Security, but you should know your options. The Social Security Administration can explain how this works.

The big mistake people make is treating retirement accounts like they would treat other assets. You can’t just withdraw the money and split it in cash. The tax consequences are severe. Always get professional help with retirement accounts.

Tax Implications and Planning

Taxes are where many people get blindsided after divorce. Understanding the basics helps you avoid costly mistakes.

Filing status changes after divorce. You can’t file as married anymore. Starting in January after your divorce is final, you’ll file as single or head of household if you have dependent children. For detailed information about how filing status affects your taxes, visit the IRS website for divorce tax information. This changes your tax brackets and deductions.

Spousal support, also called alimony, has major tax consequences. If you’re paying it, you can deduct it from your income. If you’re receiving it, you have to report it as income. This is a major difference from child support, which has no tax consequences for either parent.

Property division in divorce generally has no immediate tax consequences, but selling property later might trigger capital gains taxes. Your tax professional should review what you’re dividing to understand future tax implications.

Dependent exemptions matter if you have children. The custody arrangement usually determines who claims the exemption. This is negotiable in your divorce settlement. One parent might claim certain children while the other claims others.

College savings accounts like 529 plans need special attention because they have tax consequences if you withdraw the money. Dividing these requires careful planning.

Get Professional Help When You Need It

Some financial and legal situations are too complex to handle alone. Knowing when to get help saves you money in the long run.

A divorce attorney is essential. You might think you can do this yourself, but the financial mistakes could cost you tens of thousands of dollars. At least have an attorney review your settlement agreement before you sign it. If you need help finding a qualified divorce attorney, the American Academy of Matrimonial Lawyers provides a directory of experienced professionals in your area.

A financial advisor who specializes in divorce can help you understand your options and plan your future. They can help you figure out whether you can afford to keep the house or what your retirement will look like.

An accountant or tax professional should review your settlement agreement and help you understand tax consequences. They can also help you plan your taxes after the divorce is final.

If you have a business, you might need a business appraiser. If you have significant investments, you might need an investment specialist. If you have complex retirement accounts, a retirement account specialist can ensure you handle the division correctly.

The cost of getting professional help is usually far less than the cost of making mistakes. Don’t skip this step to try to save money.

Create Your Post Divorce Budget

Once you know what your post divorce life will look like financially, you need to create a budget. This is your roadmap for the next phase of your life.

Start with your expected income. This is what you’ll actually receive after taxes. If you’re receiving spousal support or child support, include it. If you’re unsure about receiving it consistently, create two budgets: one with it and one without.

List all your monthly expenses. Be realistic about what you actually spend. Include housing, food, transportation, insurance, childcare, medical costs, and personal expenses. Add a line for fun money because you need some flexibility in your budget.

Look at the difference between income and expenses. If your expenses are higher than your income, you need to make changes. You might need to downsize your housing, cut discretionary spending, or find ways to increase your income.

Create separate budgets for different months if your expenses vary. Maybe you spend more in winter on heating or in summer on childcare. Averaging your expenses helps you understand your true monthly costs.

Review your budget every three months for the first year after divorce. Your expenses might change as you adjust to your new situation. Your budget should change too.

Start Building Your Emergency Fund

An emergency fund is money set aside for unexpected expenses. This is critical after divorce when you’re on your own financially.

Most financial professionals recommend having three to six months of expenses in an emergency fund. For many people, this seems impossible, so start smaller. Even having one month of expenses saved helps reduce stress.

Put your emergency fund in a separate savings account that you don’t touch unless there’s a real emergency. Don’t use it for regular expenses or wants. Real emergencies include job loss, major car repairs, medical expenses not covered by insurance, or urgent home repairs.

Build your emergency fund slowly if you need to. Even putting fifty dollars per week into savings adds up to over two thousand dollars in a year. Once you have some emergency fund built, it becomes easier to handle life’s surprises.

Many people find that an emergency fund reduces stress more than almost anything else they can do. Knowing you have money set aside for unexpected problems makes the whole post divorce adjustment easier.

Update Your Legal Documents

Divorce usually means you need to update important legal documents. This protects your wishes and ensures your money goes where you want it to go.

Your will needs updating immediately. Any will that names your ex as beneficiary or executor should be changed. If you have children, make sure your will specifies who gets custody if something happens to you.

Your power of attorney document needs updating. This document says who can make financial decisions for you if you become unable to. You probably don’t want your ex having this power anymore.

Your healthcare proxy or medical power of attorney should be updated. This says who can make medical decisions for you. Again, you probably want to change this from your ex to someone you trust.

Your beneficiary designations on retirement accounts and life insurance need reviewing. These don’t pass through your will. They pass directly to whoever is named on the account. Make sure these are updated to reflect your new wishes.

Getting these documents updated takes time but is essential. Many people put this off and then face serious problems if something unexpected happens.

Conclusion: You’ve Got This

Divorce is tough emotionally and financially. The good news is that you can control your financial outcomes by following a clear plan.

Start by gathering your documents and understanding what you have and owe. Protect your credit and separate your finances. Review your insurance and housing situation. Handle retirement accounts and taxes correctly. Create a realistic post divorce budget and start building an emergency fund.

This checklist gives you a complete roadmap. You don’t need to do everything at once. Work through one section at a time and you’ll gradually gain control of your financial situation.

The financial decisions you make during and after divorce determine your security for years to come. Taking these steps now prevents mistakes that could cost you thousands of dollars later.

You’re not alone in this process. Thousands of people go through divorce every year. Many have successfully navigated these same decisions using the tools and strategies in this guide.

Start today. Pick one section from this checklist and complete it this week. Next week, move to the next section. Within a few months, you’ll have everything organized and a clear plan for your financial future.

Your post divorce life can be stable, secure, and even prosperous. All it takes is following these steps one at a time. You’ve already taken the first step by reading this guide. Now it’s time to take action.