Did you know that nearly 45% of Americans with credit scores below 620 get rejected when they apply for traditional bank loans? That’s almost half of all people who need money to buy something important like a car or furniture. If you’ve ever been turned down by a bank, you know how frustrating that feels. But there’s another option that many people don’t know about. In house financing lets you buy what you need and make payments directly to the seller. No bank required. This guide will show you exactly how it works, who can get it, and whether it’s the right choice for your situation.

What Is In House Financing?

In house financing is when you buy something and make payments directly to the store or dealer that sold it to you. Instead of getting a loan from a bank, the seller becomes your lender. They let you take home what you bought today, and you pay them back over time with interest.

Think of it like this. You want to buy a car that costs $10,000. With a traditional loan, you’d go to a bank, fill out paperwork, wait for approval, and then the bank pays the dealer. You make monthly payments to the bank. With in house financing, you skip the bank completely. The car dealer approves you right there, you sign papers with them, and you make your monthly payments directly to the dealership.

This type of financing is popular with car dealers, furniture stores, electronics shops, and even medical offices. Any business that wants to make sales easier for customers might offer it. The seller takes on more risk by lending you money, but they also make more profit from the interest you pay.

How Does In House Financing Work?

The process is pretty straightforward. You walk into a store and find something you want to buy. Maybe it’s a used car, a new bedroom set, or a washer and dryer. You tell the salesperson you’re interested in their payment plan.

They’ll ask you to fill out an application right there in the store. This usually takes about 15 to 30 minutes. You’ll need to provide basic information like your name, address, income, and where you work. Most sellers also want to see a pay stub and your driver’s license.

The seller reviews your application, often while you wait. Some places can approve you in less than an hour. Once approved, you’ll discuss the payment terms. This includes how much you’ll pay each month, how long you’ll make payments, and what interest rate they’re charging. After you agree and sign the paperwork, you can take your purchase home that same day.

You make payments every month just like any other loan. The difference is you’re sending money to the store instead of a bank. Some sellers let you pay online, while others want you to come in person or mail a check.

Who Qualifies for In House Financing?

Here’s the good news. In house financing is much easier to get than a bank loan. Most sellers care more about whether you have a job and steady income than your credit score. If you can prove you make enough money each month to cover the payments, you have a decent shot at approval.

People who typically qualify include those with bad credit, no credit history, past bankruptcies, or recent foreclosures. College students buying their first car often use in house financing. So do people who are rebuilding their credit after financial problems.

Each seller sets their own requirements, so what gets you approved at one place might not work somewhere else. Most want to see that you’ve been at your job for at least a few months. They also like when you can make a down payment because it shows you’re serious and reduces their risk.

You’ll usually need to bring proof of income like recent pay stubs, proof of where you live like a utility bill, valid identification, and references who can vouch for you. Some sellers also want to see your bank statements to verify you have some money coming in regularly.

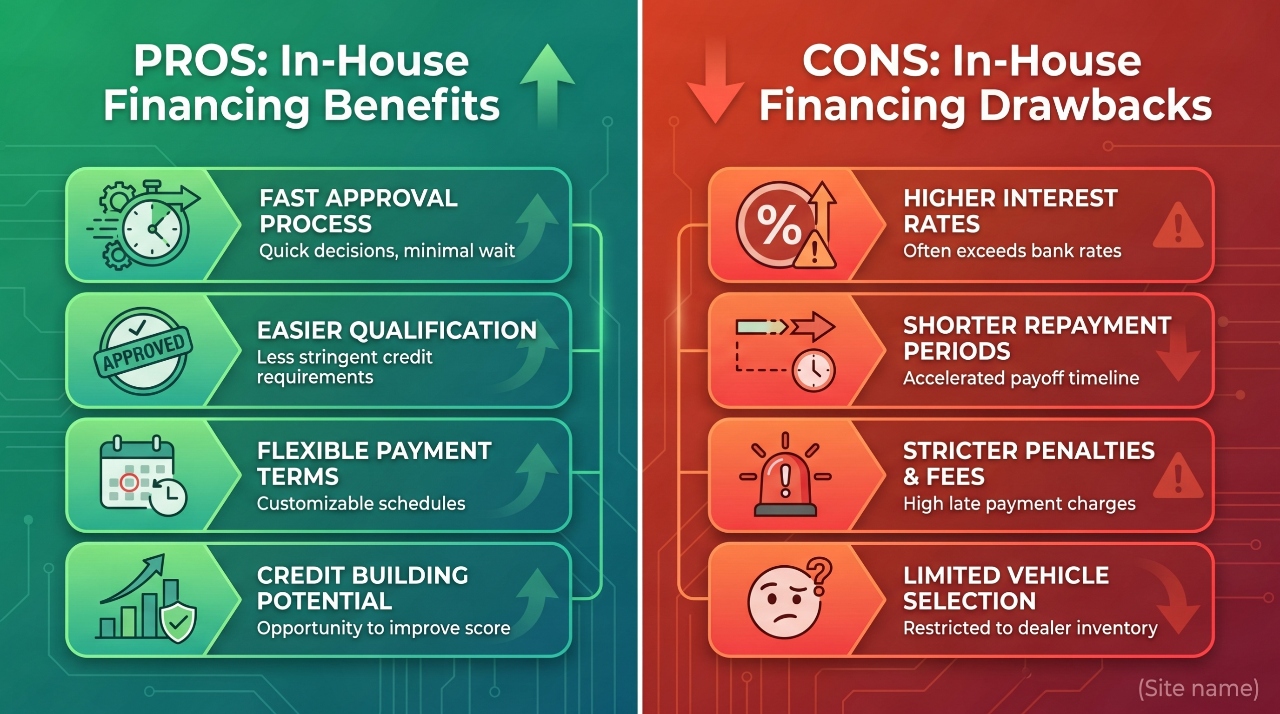

The Benefits of In House Financing

The biggest advantage is speed. Banks can take days or even weeks to approve a loan. With in house financing, you can walk in with bad credit and drive out in a car the same day. When you need something urgently, that speed matters a lot.

Bad credit doesn’t automatically disqualify you. Traditional lenders have strict credit score requirements that knock out millions of people. In house financing sellers look at your whole picture. They want to know if you have income and stability, not just a number from a credit bureau. This opens doors for people who banks won’t help.

Everything happens in one place, which makes life simpler. You shop, get approved, and set up payments all in the same building. There’s no running back and forth between the bank and the store. You deal with one company for everything related to your purchase.

Terms can be more flexible too. Banks have rigid rules about loan amounts and payment schedules. A seller might work with you to create a payment plan that fits your budget. Need smaller payments stretched over more time? They might do it. Want to pay more upfront to lower your monthly amount? That’s often possible.

Some sellers report your payments to credit bureaus. If they do, making your payments on time actually helps rebuild your credit score. After a year or two of good payments, you might qualify for better financing options. This turns in house financing into a stepping stone toward financial recovery.

The Drawbacks You Should Know

Nothing is perfect, and in house financing has real downsides you need to understand. The interest rates are almost always higher than what banks charge. Where a bank might charge 5% to 8% interest, an in house financing deal might charge 15% to 25% or even more. Over time, this means you pay a lot more for the same item.

Your selection is limited to whatever that one seller has available. If you’re buying a car through a buy here pay here dealer, you can only choose from their lot. You can’t shop around at other dealers and bring financing with you like you could with a bank loan.

Loan terms are often shorter. A bank might give you five or six years to pay off a car. In house financing might require you to pay it off in two or three years. Shorter terms mean higher monthly payments, which can strain your budget.

Miss a payment and you’ll face strict penalties. Many sellers charge late fees that add up fast. Some will repossess your car or take back your furniture after just one or two missed payments. Banks usually give you more chances and time to catch up. Sellers who offer in house financing often move quickly to protect their investment.

You might have fewer legal protections depending on the contract structure. Some consumer protection laws apply differently to in house financing versus traditional loans. Always read the fine print and understand what rights you have.

The biggest risk is losing what you bought. If you finance a car and miss payments, the dealer can repossess it. You lose the car and all the money you already paid. Some contracts are structured so you don’t build any equity until near the end of the payment term.

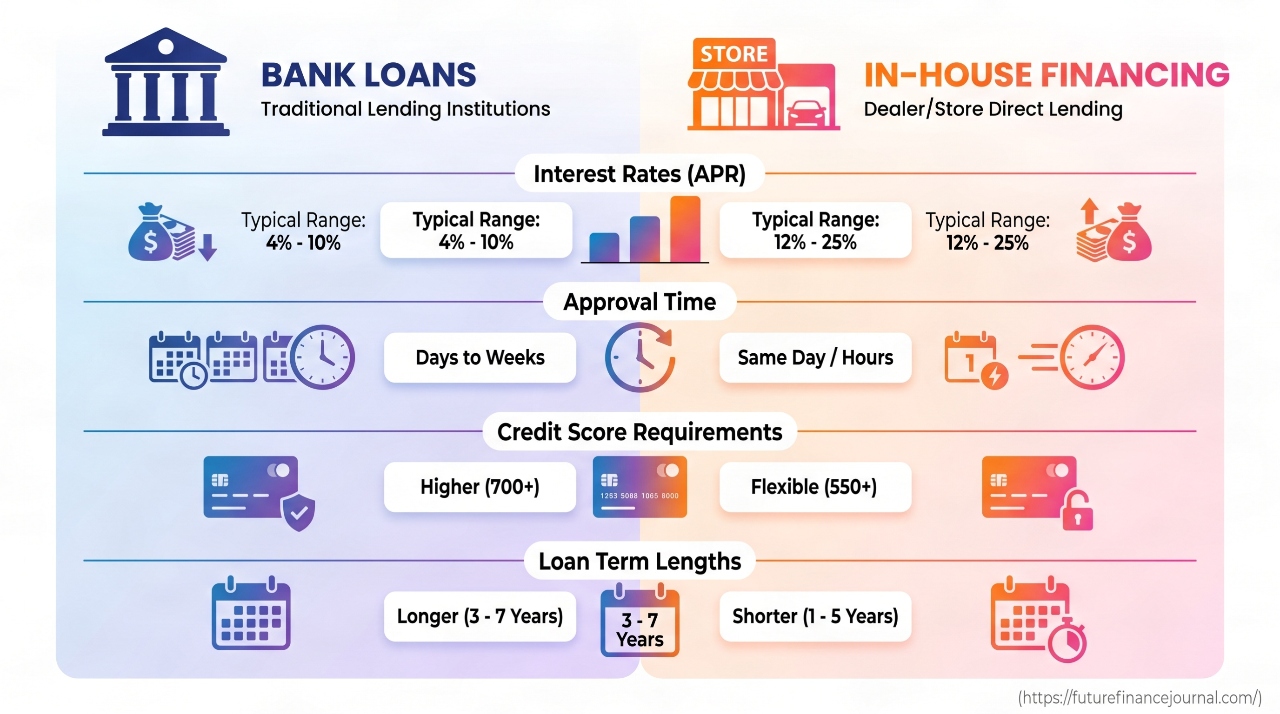

In House Financing vs Traditional Loans

Understanding the differences helps you make a smart choice. Traditional bank loans offer lower interest rates, sometimes half of what in house financing charges. You get longer repayment periods, which means smaller monthly payments that fit easier into your budget. Banks give you a check or transfer that you can use at any seller, so you shop around for the best deal.

The approval process takes longer though. You might wait three days to two weeks for a decision. Banks have strict credit requirements that eliminate many applicants. They want to see stable employment history, low debt compared to your income, and a good credit score.

In house financing gives you an answer in hours, not days. Credit requirements are relaxed or almost nonexistent. You handle everything in one location. The tradeoff is higher interest rates, shorter loan terms, and limited shopping options. You pay more money overall but get access when banks say no.

Here’s a simple comparison. A $15,000 car loan from a bank at 6% interest over five years costs you about $2,400 in interest. The same car through in house financing at 20% interest over three years costs you about $5,000 in interest. You pay more than double in interest charges, but you get the car when a bank won’t approve you.

Common Industries That Offer In House Financing

Car dealerships use in house financing more than any other industry. Buy here pay here lots specialize in selling to people with credit problems. They typically sell used cars and handle all the financing themselves. You pick a car, get approved on the spot, and drive away. Weekly or biweekly payments are common, and the dealer can disable your car remotely if you stop paying.

Furniture stores have offered payment plans for decades. You can furnish your whole apartment and pay over 12 to 36 months. Some furniture deals come with zero interest if you pay everything off within a promotional period, but miss that deadline and they charge you interest going back to day one.

Electronics retailers let you finance computers, phones, TVs, and appliances. Rent to own stores are a version of in house financing where you make payments until you own the item. These deals often cost double or triple the retail price when you add up all the payments.

Medical and dental offices know that health care is expensive. Many offer payment plans for procedures that insurance won’t cover. You might finance dental work, plastic surgery, or fertility treatments directly through the doctor’s office. Interest rates vary widely, and some offices charge no interest if you pay within a certain timeframe.

Jewelry stores commonly finance engagement rings and expensive watches. You can propose now and pay later. Terms usually run from six months to three years depending on the purchase price. The interest rates can be high, so read the contract carefully.

HVAC companies and home improvement contractors offer financing for new air conditioners, furnaces, roofs, and kitchen remodels. These are big ticket items that most people can’t pay for all at once. Contractor financing helps you get the work done now and spread payments over time.

How to Get Approved for In House Financing

Preparation increases your chances. Bring recent pay stubs from the last month to prove your income. Having two or three stubs looks better than just one. If you’re self employed, bring bank statements showing regular deposits.

Save up for a down payment if possible. Even $500 or $1,000 shows you’re committed and reduces the amount you need to finance. Larger down payments sometimes get you better terms or higher approval odds.

Have your driver’s license or state ID ready. Sellers need to verify who you are. Bring proof of your current address like a recent utility bill or lease agreement. Your name and address should match on all documents.

Prepare a list of references with their phone numbers. These should be people who know you’re responsible, like employers, landlords, or long time friends. Don’t use family members as references unless the seller specifically allows it.

Be completely honest on your application. Lying about your income or job history will get you denied or cause problems later. Sellers verify the information you provide. Getting caught in a lie means automatic rejection.

Show stability whenever possible. If you’ve been at the same job for a year or more, that helps. Living at the same address for a while looks good too. Frequent job changes or moving around makes sellers nervous about whether you’ll make payments.

Questions to Ask Before You Sign

Never sign papers without getting clear answers to important questions. Understanding the deal protects you from nasty surprises later.

What is the total amount I’ll pay over the life of this agreement? This includes the price, interest, and all fees. Knowing the true cost helps you decide if it’s worth it.

What interest rate are you charging me? Get the actual percentage, not just the monthly payment amount. Some sellers avoid telling you the rate because it’s shockingly high.

How long is my payment term? Know whether you’re paying for one year, three years, or five years. Shorter terms mean higher monthly payments.

Are there penalties if I pay off the loan early? Some contracts charge you extra for paying everything off ahead of schedule, which seems unfair but is legal in many places.

What fees do you charge besides interest? Look for origination fees, documentation fees, late payment fees, and processing fees. These add up quickly.

Do you report my payments to the credit bureaus? If they don’t report, making on time payments won’t help rebuild your credit.

What exactly happens if I miss a payment? Learn about grace periods, late fees, and when they’ll repossess or take back what you bought.

Can I return the item if I change my mind? Most in house financing is final, but some sellers have a short return window.

What warranty or guarantee comes with my purchase? Used cars and electronics sometimes break. Know what’s covered and for how long.

Is there anything required that costs extra? Some car dealers require you to buy gap insurance or extended warranties as a condition of financing. These add to your costs.

Red Flags to Watch Out For

Some sellers use in house financing to take advantage of desperate people. Learn to spot the warning signs. High pressure tactics are a major red flag. If someone pushes you to sign today because the deal expires tonight, walk away. Legitimate offers will still be there tomorrow.

A seller who won’t clearly explain the terms is hiding something. You deserve to understand everything before you commit. If they talk fast, use confusing language, or refuse to show you the numbers in writing, leave.

Watch for fees that seem excessive or don’t make sense. A $500 documentation fee to process paperwork might be a junk fee designed to increase their profit. Ask what each fee covers and whether it’s negotiable.

Interest rates above 25% should make you very cautious. Yes, in house financing costs more than bank loans, but there are limits to what’s reasonable. Some rates cross into predatory lending territory.

Required add-ons that you don’t want or need are another warning sign. Forcing you to buy an expensive warranty or insurance policy as a condition of financing might be illegal depending on your state.

Vague contract language that doesn’t specify exact terms means you can’t hold them accountable later. Everything should be spelled out clearly in writing.

No cooling off period or right to cancel is concerning. Some states require a few days where you can change your mind. If the seller pressures you to waive this right, ask yourself why.

Tips for Managing Your In House Financing

Once you’re approved and have your purchase, managing the payments correctly is critical. Make every payment on time, every single month. Set up automatic payments if the seller allows it. Late payments trigger fees and could lead to repossession.

Pay more than the minimum whenever you can. Extra money goes toward the principal balance, which reduces the total interest you pay. Even an extra $20 or $50 per month makes a difference over time.

Keep every receipt, statement, and piece of paper related to your financing. Store them in a folder or take photos and keep digital copies. If there’s ever a dispute about payments, you’ll have proof.

Contact the seller immediately if you’re going to have trouble making a payment. Don’t just skip it and hope they won’t notice. Many sellers will work with you if you communicate. They might let you pay late without reporting it or adjust your payment schedule temporarily.

Review your statements every month to make sure payments are credited correctly. Mistakes happen, and you want to catch them early. Verify that your balance is going down as expected.

If your credit improves during the payment term, consider refinancing with a bank or credit union. You might get a much lower interest rate and save thousands of dollars. Some in house financing contracts allow early payoff without penalty, making refinancing possible.

What Happens If You Can’t Make Payments?

Missing payments creates serious problems fast. The seller will contact you, usually within a few days of a missed payment. They want their money and will call, text, or email repeatedly. Ignoring them makes everything worse.

Late fees get added to your balance. These might be $25, $50, or even more per missed payment. Multiple late fees pile up and make it even harder to catch up.

Your credit score drops if the seller reports to credit bureaus. Each missed payment stays on your credit report for seven years. This makes it harder to get approved for anything in the future.

Repossession happens quickly with in house financing. Unlike banks that might wait 60 or 90 days, some sellers will take back a car after just two or three missed payments. They can show up at your home or job and tow the vehicle away. You lose the car and all the money you already paid.

For furniture or electronics, the seller might sue you in court to get the items back or get a judgment for the money you owe. Court judgments damage your credit even more and can lead to wage garnishment.

Your best option is always to communicate before you miss a payment. Explain your situation and ask for help. Some sellers will let you skip a payment and add it to the end of the loan. Others might reduce your payment amount temporarily. They’d rather work with you than go through the hassle of repossessing items and reselling them.

Alternatives to In House Financing

In house financing isn’t your only option, even with bad credit. Credit unions are more flexible than big banks and often approve people who banks reject. Their interest rates are much lower than in house financing. If you have bad credit, look for credit unions that specialize in helping people rebuild.

Personal loans from online lenders have become popular. Companies like Upstart or OneMain Financial approve people with lower credit scores. The rates are still high but usually better than in house financing. You get cash that you can spend anywhere.

Credit cards designed for people with bad credit are another possibility. Secured credit cards require a deposit but approve almost everyone. You won’t buy a car with a credit card, but you might finance furniture or electronics.

Peer to peer lending platforms connect borrowers with individual investors. Your loan request gets posted and people decide whether to fund it. Interest rates vary based on your credit, but approval odds are decent.

Getting a cosigner with good credit dramatically improves your approval chances at traditional banks. A cosigner agrees to pay if you don’t. This lowers the risk for the lender. Parents or other family members sometimes cosign to help you get started.

Layaway programs let you pay over time and take the item home when it’s paid off. You don’t pay interest, but you don’t get to use what you’re buying until you’ve paid in full. This works better for things you want but don’t need immediately.

Saving up to pay cash is always the cheapest option. It requires patience and discipline, but you avoid interest completely. Even saving for a few months to increase your down payment reduces how much you need to finance.

Real Stories: When In House Financing Makes Sense

Jennifer had filed for bankruptcy two years earlier after medical bills piled up. No bank would approve her for a car loan, but she landed a good job 15 miles from her apartment. Without a car, she’d lose the job. A buy here pay here dealer approved her the same day. She paid 22% interest, which was high, but she kept the job and made every payment on time. After two years, her credit score improved enough to refinance with a credit union at 9% interest.

Marcus moved to a new city for college with no credit history at all. He needed furniture for his apartment but had been in the country only three years and never had a loan or credit card. The furniture store offered in house financing with no credit check. He bought a bed, desk, and couch for $2,000 and paid it off over 18 months. The store reported his payments to the credit bureaus, which helped him build credit for the first time.

Sarah’s air conditioner died in July during a heat wave. She had $500 in savings but needed a new unit that cost $4,500. The HVAC company offered financing at 18% interest over three years. She could have tried to get a personal loan, but that would take a week and she had two small kids suffering in 95 degree heat. She took the in house financing to get cool air immediately. Once things settled down, she made extra payments and paid it off in 18 months instead of three years.

Conclusion

In house financing gives people access to things they need when traditional lenders say no. The approval process is fast and the credit requirements are minimal. For someone in a tough spot who needs a car to get to work or furniture to make an apartment livable, it can be a lifeline. The costs are real though. You’ll pay significantly more in interest compared to bank loans. The terms are stricter and the risk of losing what you bought is higher if you miss payments.

This financing works best as a short term solution. Use it to get what you need now while you work on improving your credit and financial situation. Make every payment on time to avoid fees and repossession. Look for chances to refinance or pay it off early. Understand every detail of the contract before you sign. Ask questions until you’re completely clear on what you’re agreeing to. Compare the total cost with other options even if you think you won’t qualify.

In house financing isn’t good or bad by itself. It’s a tool that helps some people and costs others dearly. Your job is to figure out which group you’ll be in.