Over 50 million Americans use Cash App, but most don’t know which actual bank holds their money. This matters more than you think, especially when setting up direct deposit or receiving wire transfers. Your boss needs this information to pay you. The IRS needs it to send your tax refund. Without knowing your cash app banking name, you could miss out on payments or face frustrating delays.

Cash App isn’t technically a bank itself. It partners with real banks to hold your money and provide banking services. This setup affects everything from how you receive direct deposits to how your funds stay protected. Many people assume Cash App is just a payment app, but it offers actual banking features through these partnerships. Understanding which bank handles your account helps you use Cash App more effectively and answers important questions when employers or government agencies ask for your banking details.

This guide explains exactly which banks work with Cash App, how to find your specific banking name, and why this information matters for your daily finances.

The Quick Answer: What Bank Does Cash App Use?

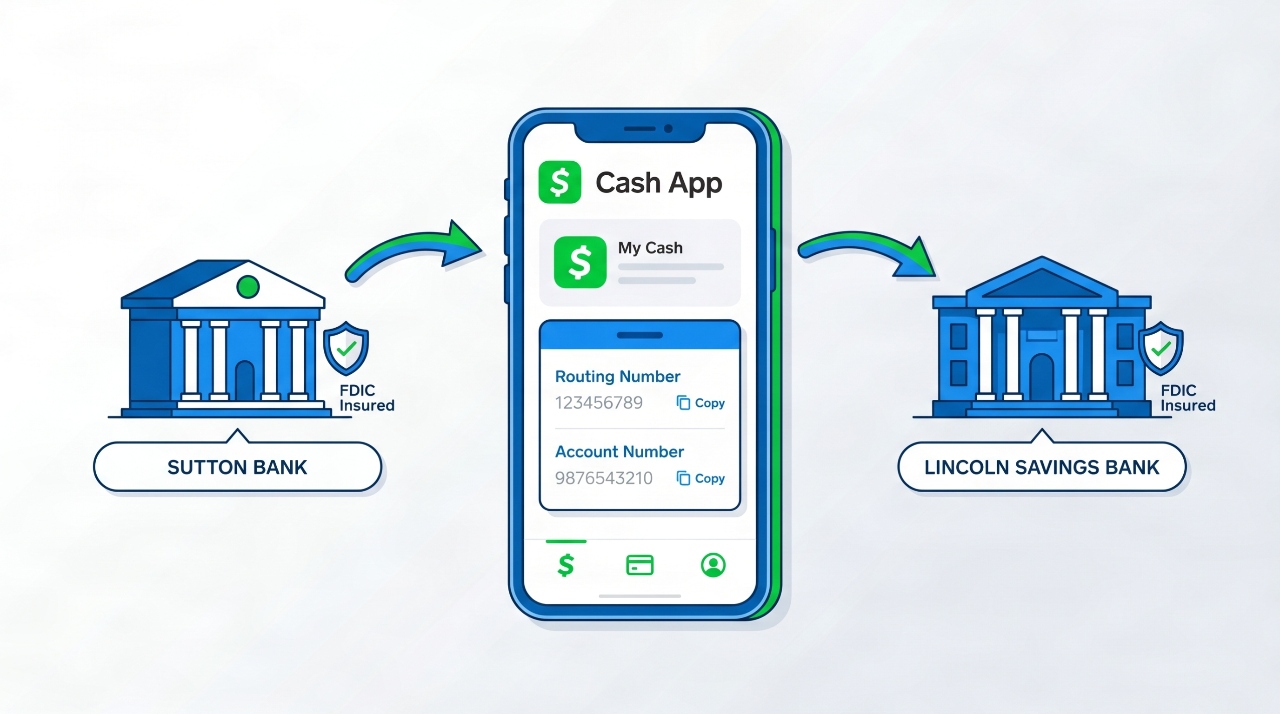

Cash App partners with two banks: Sutton Bank and Lincoln Savings Bank. Your account connects to one of these two institutions. Which one you get depends on when you signed up and where you live. Cash App assigns your banking partner automatically when you create your account.

You cannot choose between Sutton Bank and Lincoln Savings Bank. The assignment happens behind the scenes based on Cash App’s internal distribution system. Both banks provide identical services and protections for Cash App users. Your experience remains the same regardless of which bank holds your funds.

Cash App uses partner banks instead of becoming a bank itself because of regulations. Getting a banking license requires years of applications, massive capital reserves, and ongoing compliance costs. The partnership model lets Cash App offer banking features without these burdens. Many fintech companies use this same approach. Chime, Varo, and other digital apps partner with traditional banks rather than obtaining their own licenses.

Sutton Bank: One of Cash App’s Banking Partners

Sutton Bank operates out of Attica, Ohio, where it has served customers since 1892. This community bank has over 130 years of history and became an FDIC member in 1934. Despite its small town roots, Sutton Bank works with numerous fintech companies as a banking partner.

Cash App chose Sutton Bank because of their experience with digital banking partnerships. Sutton Bank already worked with several payment apps and prepaid card programs before teaming up with Cash App. They handle the regulatory requirements and banking infrastructure while Cash App focuses on the user experience and app development.

When Sutton Bank is your cash app banking partner, your money sits in accounts maintained by this Ohio institution. The bank processes your direct deposits, manages your routing and account numbers, and ensures regulatory compliance. You never interact with Sutton Bank directly. Everything happens through the Cash App interface you already know.

FDIC insurance covers your Cash App balance up to $250,000 when Sutton Bank holds your account. This protection means your money stays safe even if Cash App shuts down or faces financial problems. The federal government backs this insurance, giving you the same protection as any traditional bank account.

Lincoln Savings Bank: Cash App’s Other Banking Partner

Lincoln Savings Bank is located in Reinbeck, Iowa, a small community where the bank has operated since 1902. Like Sutton Bank, Lincoln Savings Bank is an FDIC member with a long history of traditional banking. They entered the fintech partnership space to diversify their business and serve modern banking needs.

Lincoln Savings Bank provides identical services to Cash App users as Sutton Bank does. They maintain your account details, process deposits and withdrawals, and handle regulatory requirements. The bank name appears on your Cash App banking details, but you manage everything through the app itself.

Cash App distributes users between its two banking partners based on capacity and regional factors. Some users get assigned to Sutton Bank while others connect to Lincoln Savings Bank. This distribution helps Cash App scale its services without overloading a single banking partner.

The same $250,000 FDIC insurance applies whether Sutton Bank or Lincoln Savings Bank holds your account. Both institutions maintain the same security standards and regulatory compliance. Your cash app banking name changes, but your protections and features remain identical.

How to Find Out Which Bank Holds Your Cash App Account

Finding your cash app bank name takes less than a minute. Open the Cash App on your phone and tap the profile icon in the upper corner. This icon looks like a silhouette or shows your profile picture if you added one.

Next, tap on “Personal” or select your displayed balance. The app shows your account details including your routing number and account number. The banking name appears right above or below these numbers.

Your routing number tells you which bank holds your account even before you see the name. Sutton Bank uses routing number 041215663 for all Cash App accounts. Lincoln Savings Bank uses routing number 073923033. These nine digit codes identify the financial institution in the banking system.

Write down your routing number, account number, and bank name somewhere safe. You need this information when setting up direct deposit with employers. Government agencies ask for these details when sending benefits or tax refunds. Some bill payment services require your banking information for automatic withdrawals.

Your cash app routing number never changes unless Cash App switches your account to a different banking partner, which rarely happens. The account number stays with you as long as you keep your Cash App account active. Store this information in a password manager or secure note on your phone.

Why Cash App Uses Partner Banks Instead of Being Its Own Bank

Banking regulations in the United States are strict and expensive to follow. A company must apply for state and federal banking licenses, which costs millions of dollars and takes years to obtain. Banks need substantial capital reserves just sitting idle to meet regulatory requirements. They face ongoing examinations, audits, and compliance costs.

Cash App chose the partnership model to avoid these obstacles. By working with established banks, Cash App can offer banking features without the regulatory burden. This approach lets the company move faster and add new features more quickly than traditional banks can.

The benefits of this model extend to users too. Cash App keeps costs down by not maintaining expensive banking infrastructure. These savings translate to no monthly fees for basic accounts. The app can focus on user experience and technology instead of regulatory paperwork.

Most fintech apps follow the same pattern. Venmo partners with The Bancorp Bank. PayPal works with multiple banking partners depending on the service. Chime uses Stride Bank and The Bancorp Bank. This partnership approach has become the standard way digital payment apps offer banking services.

Cash App still provides FDIC insurance despite not being a bank itself. The protection comes from Sutton Bank and Lincoln Savings Bank, both legitimate FDIC members. Users get the same safety as opening an account directly with these banks.

The partnership also gives Cash App access to traditional banking infrastructure. Wire transfers, ACH payments, and check processing all run through established banking networks. Sutton Bank and Lincoln Savings Bank handle these connections while Cash App provides the modern interface.

What This Banking Partnership Means for Your Money

FDIC insurance protects your Cash App balance up to $250,000. This coverage applies to the money sitting in your Cash App account, including your Cash App balance and savings. If Sutton Bank or Lincoln Savings Bank fails, the federal government reimburses you for covered losses.

Your funds stay separate from Cash App’s corporate money. The banking partners maintain your deposits in accounts distinct from the company’s operating funds. This separation protects you if Cash App faces bankruptcy or legal problems. The bank holds your money in trust, meaning it belongs to you, not Cash App.

Understanding these protections helps you decide how much money to keep in Cash App. The $250,000 limit covers most people’s daily banking needs. However, if you regularly keep more than this amount in your account, consider splitting funds across multiple institutions.

Some Cash App features don’t qualify for FDIC insurance. Bitcoin held in your Cash App account is not insured because cryptocurrency isn’t a deposit. Stocks purchased through Cash App Investing have SIPC protection instead of FDIC coverage. Only the cash balance in your regular Cash App account gets FDIC protection.

Your cash app savings account earns interest while maintaining FDIC insurance. The rates change based on market conditions and promotions. Some users get boosted rates as incentives. All savings balances count toward your $250,000 insurance limit along with your regular Cash App balance.

The banking partnership means you can use Cash App like a checking account for many purposes. Direct deposit works the same way as traditional banks. You can receive ACH transfers from other institutions. Wire transfers come through using your routing and account number.

When You Need Your Cash App Banking Name

Setting up direct deposit with your employer requires your cash app bank name, routing number, and account number. Your HR department needs these details to send your paycheck to Cash App. Most employers accept Cash App as a valid direct deposit destination, but some might ask questions because they don’t recognize Sutton Bank or Lincoln Savings Bank.

Tax refunds from the IRS can go straight to your Cash App account using your banking details. When filing your taxes, enter your routing number and account number in the refund section. The IRS treats Cash App like any other bank account. Refunds typically arrive within the standard timeframe, and Cash App users often get their money up to two days early.

Government benefits including Social Security, unemployment insurance, and stimulus payments work with Cash App direct deposit. Provide your banking information to the relevant agency. These payments process through the same ACH network as employer deposits.

Wire transfers require your cash app banking name and account details. If someone wants to wire you money, they need your routing number, account number, and the bank name. International wires might need additional information like SWIFT codes. Contact Cash App support for these details since they vary by situation.

Automatic bill payments sometimes require your banking information. Utility companies, loan servicers, and subscription services can pull payments directly from your Cash App account. Set this up through the biller’s website using your routing and account numbers. Make sure you maintain sufficient balance to avoid failed payments.

Linking Cash App to other financial apps or services needs your banking details. Budgeting apps like Mint or YNAB can connect to your Cash App account. Investment platforms might let you fund purchases from Cash App. These connections use your routing and account numbers to establish secure links.

Employers may hesitate when they see Sutton Bank or Lincoln Savings Bank because they’re not household names. Assure them both banks are legitimate FDIC institutions. Provide your routing and account numbers exactly as they appear in Cash App. Most payroll systems accept these details without problems once you confirm the information is correct.

Common Problems and How to Fix Them

Some employers don’t recognize Sutton Bank or Lincoln Savings Bank by name. They worry about sending paychecks to unfamiliar institutions. Explain that these banks partner with Cash App and are FDIC insured. Show your HR department the banking details directly from your Cash App account. Most concerns disappear once they verify the routing number in their banking database.

Direct deposit rejection happens occasionally for various reasons. Double check that you entered your routing and account numbers correctly. A single wrong digit causes the deposit to fail. Verify the numbers match exactly what appears in your Cash App settings. Contact your employer’s payroll department to confirm they entered the information properly on their end.

Some payroll systems flag Cash App accounts as prepaid cards rather than checking accounts. This classification can cause automatic rejections. Ask your HR department to override this flag or mark your account as a checking account. Most systems allow manual overrides when the employee confirms their banking details.

Failed direct deposits usually bounce back to the sender within a few business days. You won’t lose the money, but you’ll experience delays getting paid. Fix the underlying problem before the next pay period. Update your banking information if anything changed or if you discovered errors in the original entry.

Wrong banking information gets corrected through your employer or the sending institution. You cannot change how payments route once they’re sent. Contact Cash App support if a deposit hasn’t arrived when expected. They can track incoming transfers and identify problems. Support can also confirm your current routing and account numbers if you’re unsure about the details.

Cash App sometimes updates account numbers for security reasons or system changes. Check your banking details before setting up new direct deposits. Don’t assume the numbers you used months ago are still current. The routing number changes only if Cash App switches you to a different banking partner, which happens rarely.

Cash App Banking Services Available

Direct deposit through Cash App gets you paid up to two days early. Employers typically send payroll files to banks a few days before payday. Traditional banks hold these funds until the official pay date. Cash App releases the money as soon as they receive it from your employer. This feature alone makes Cash App attractive for people living paycheck to paycheck.

Savings accounts on Cash App earn interest on your balance. The rates vary and sometimes include promotional boosts. Cash App savings have no minimum balance requirements and no monthly fees. You can move money between your regular balance and savings instantly within the app.

The Cash Card works as a debit card linked to your Cash App balance. Use it anywhere Visa is accepted. The card is free with no activation fees. Custom designs let you personalize your card’s appearance. Cashback rewards apply at select merchants, giving you money back on purchases.

ATM access comes through the Cash Card at supported machines. Free withdrawals at select ATMs let you get cash without fees. Other ATMs might charge their own fees, which Cash App displays before you complete the transaction. You can withdraw up to specific daily limits depending on your account status.

Mobile check deposit lets you add money to Cash App by photographing checks. The app processes the check and adds funds to your balance, usually within a few business days. Limits apply based on your account history and verification level.

Person to person transfers happen instantly between Cash App users. Send money to friends, split bills, or pay people back. These transfers are free when using your Cash App balance or linked bank account. Credit card transfers incur a small fee.

Cash App lacks physical branches, which bothers people who prefer face to face banking. You handle everything through the app or website. Customer service happens via email, chat, or phone. This setup works great for tech comfortable users but frustrates people who want in person help.

No paper checks are available with Cash App accounts. You cannot order a checkbook or write checks against your balance. This limitation doesn’t matter to most users, but some situations still require paper checks. Keep a traditional bank account if you regularly need checks.

Fee structures differ from traditional banks in important ways. Cash App charges no monthly maintenance fees and no overdraft fees. However, instant transfers to your bank account cost a small percentage. ATM fees apply at out of network machines. Bitcoin transactions include spreads and fees. Understanding these costs helps you use Cash App efficiently.

Security and Safety of Your Banking Information

Cash App encrypts your banking details using industry standard technology. Your routing number, account number, and personal information stay protected during transmission and storage. The app uses the same encryption banks use for online banking.

Two factor authentication adds extra security to your account. Enable this feature in your settings to require a code when logging in from new devices. This protection prevents unauthorized access even if someone steals your password.

Sutton Bank and Lincoln Savings Bank maintain bank level security for all Cash App accounts. Both institutions follow federal regulations for data protection and privacy. Regular audits ensure compliance with banking security standards. Your money benefits from the same protections as traditional bank accounts.

Users should create strong, unique passwords for their Cash App accounts. Don’t reuse passwords from other services. A password manager helps you generate and store complex passwords safely. Change your password immediately if you suspect your account was compromised.

Enable notifications for all transactions. Cash App can alert you instantly when money moves in or out of your account. These alerts help you catch unauthorized activity quickly. Review your transaction history regularly to verify all activity is legitimate.

Never share your Cash App PIN or password with anyone. Cash App employees will never ask for this information. Scammers often pose as support staff to trick users into revealing login details. Contact support only through official channels within the app.

Your cash app bank details are safe to share with legitimate employers and institutions. The routing and account numbers are meant to be shared for direct deposit purposes. However, keep your Cash App login information private. Anyone with your password can access your account and steal your money.

Comparing Cash App to Traditional Banks

Traditional banks offer physical locations where you can speak with employees face to face. This access helps when you need complex services or have problems requiring personal attention. Cash App has no branches, which saves them money but limits your support options.

Customer service at traditional banks happens in person, by phone, or online. You often get dedicated account representatives. Cash App support operates primarily through chat and email. Response times vary, and complex problems sometimes take longer to resolve.

Traditional banks provide more services overall. Business accounts, loans, credit cards, safe deposit boxes, and investment services come standard. Cash App focuses on basic banking and payments. You might need additional accounts elsewhere for comprehensive financial needs.

Transaction limits at traditional banks are generally higher than Cash App. Large wire transfers, big check deposits, and substantial daily spending work better at established banks. Cash App limits increase as you verify your account and build history, but caps still exist.

Cash App charges no monthly maintenance fees for basic accounts. Traditional banks often require minimum balances or charge monthly fees. These costs add up over time. Cash App’s fee free structure benefits people who maintain lower balances.

Instant transfers between Cash App users happen free and immediately. Traditional banks charge for wire transfers and process ACH payments over several days. This speed makes Cash App better for splitting bills and paying friends.

Mobile first design makes Cash App easier to use on smartphones. The interface focuses on quick, simple transactions. Traditional bank apps often feel clunky because they’re adapted from desktop systems. Cash App built its experience for phones from the start.

Account setup takes minutes with Cash App. Download the app, enter basic information, and start using your account. Traditional banks require appointments, paperwork, and identity verification that can take days. This convenience helps people who need banking access immediately.

Use Cash App as your primary bank if you’re comfortable with mobile only banking and don’t need extensive services. It works well for direct deposit, daily spending, and basic savings. Keep a traditional bank account alongside Cash App if you need services like loans, safe deposit boxes, or prefer having physical branch access.

Frequently Asked Questions

Can I choose between Sutton Bank and Lincoln Savings Bank?

No, Cash App assigns your banking partner automatically when you create your account. You cannot switch between banks or select your preference.

Will my banking name ever change?

Banking partners rarely change for existing accounts. Cash App might migrate users between banks during major system updates, but this happens infrequently. You’ll receive notice if your banking details change.

Do I need different information for different types of deposits?

No, use the same routing number and account number for all deposits. Direct deposits, wire transfers, and ACH payments all use these same details.

Is there a limit to how much money I can keep in Cash App?

Cash App has balance limits that increase with account verification. FDIC insurance covers up to $250,000. Check your specific account limits in the app settings.

Can I open multiple Cash App accounts?

Cash App allows one personal account per person. You cannot open multiple personal accounts. However, you can have both a personal account and a business account if you run a company.

Conclusion

Your cash app banking name is either Sutton Bank or Lincoln Savings Bank, depending on which partner Cash App assigned to your account. Both banks are legitimate, FDIC insured institutions that provide identical services and protections. Your experience remains the same regardless of which bank holds your funds.

Knowing your specific cash app bank name matters when setting up direct deposit with employers, receiving tax refunds, or getting government benefits. This information is easy to find in your Cash App settings alongside your routing and account numbers. Keep these details stored securely for when you need them.

Cash App offers real banking features through these partnerships while maintaining the convenience and simplicity of a mobile app. The FDIC insurance protects your money just like traditional bank accounts. Understanding how these partnerships work helps you use Cash App confidently and effectively.

Open your Cash App right now and check which bank holds your account. Tap your profile, select your balance or personal information, and find your routing number and bank name. Write down these details in a safe place like a password manager or secure note. You’ll thank yourself later when your employer asks for direct deposit information or when you need to receive an important payment.