In 2022, Indian companies raised over $2.3 billion through compulsory convertible debentures, making them one of the fastest growing financing tools in emerging markets. Yet most everyday investors have never heard of them. This guide explains what compulsory convertible debentures are, why companies use them, and whether they fit your investment goals.

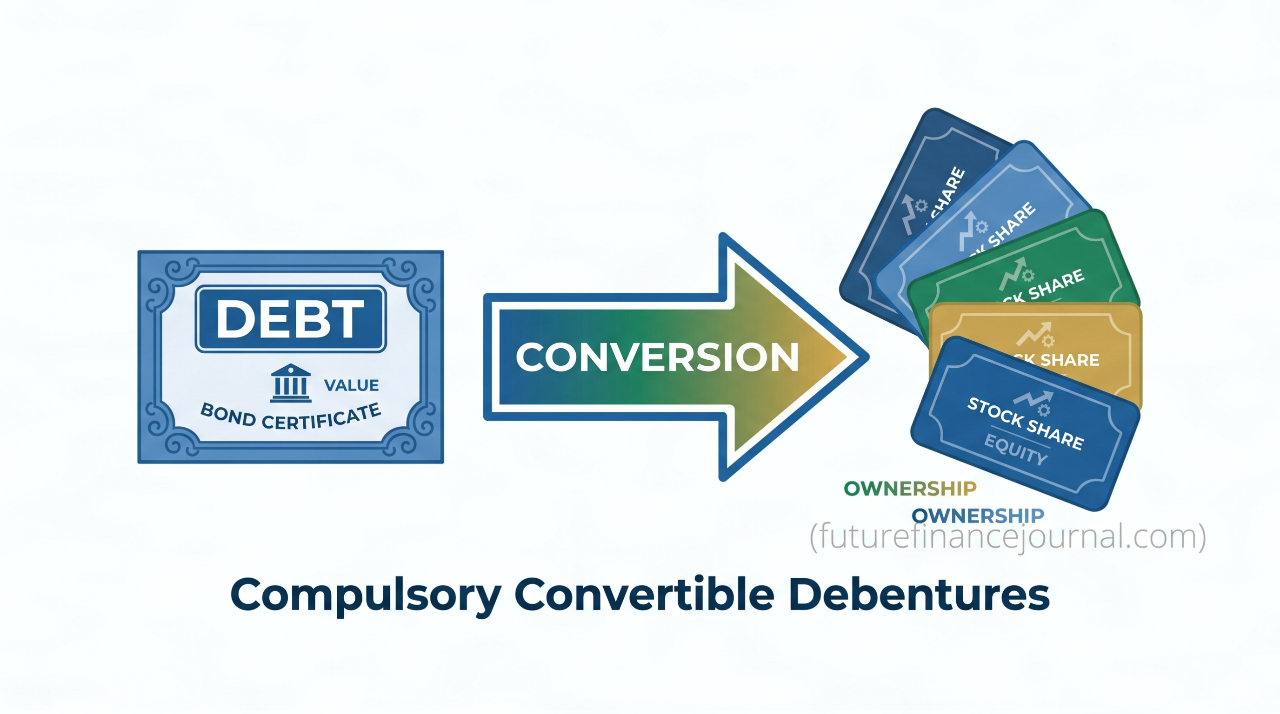

Think of a compulsory convertible debenture as a loan that automatically becomes stock. You lend money to a company, receive regular interest payments, and then at a set date, your loan converts into shares whether you like it or not. The “compulsory” part is important—you do not get to choose.

What Are Compulsory Convertible Debentures?

A compulsory convertible debenture is a financial instrument that sits between a bond and stock. When you buy one, you are essentially giving a company a loan. The company promises to pay you interest regularly, just like a regular bond. But here is the twist: on a predetermined date, your debenture automatically converts into company shares.

The word “compulsory” means mandatory. You cannot decide to keep your debenture as debt. Conversion happens automatically according to the terms stated when the debenture was issued. This makes CCDs fundamentally different from optional convertible debentures, where investors can choose whether to convert or stay as debt holders.

Let us look at a simple example. Suppose you buy a CCD with a face value of 1,000 rupees at an interest rate of 8 percent. You receive 80 rupees in interest each year. After five years, the debenture automatically converts into shares based on a conversion ratio set by the company. You now own equity instead of debt, regardless of whether you wanted that outcome.

The Basic Features of CCDs

Compulsory convertible debentures have several defining characteristics that set them apart. Understanding these features helps you evaluate whether CCDs match your investment style.

Fixed Conversion Date: Every CCD has a mandatory conversion date written into the terms. This could be three years away, five years away, or even longer. You know exactly when your debt becomes equity. There is no flexibility or optionality on this date.

Predetermined Conversion Ratio: Before you invest, the company states how many shares you will receive per debenture. If the conversion ratio is 1:5, each debenture converts into five shares. This ratio stays fixed regardless of what happens to the stock price.

Regular Interest Payments: Until conversion occurs, you receive periodic interest, usually semi-annually or annually. These payments continue as long as your investment remains in debenture form.

Mandatory Conversion: You cannot request early conversion or ask to stay as a debt holder. When the maturity date arrives, conversion happens automatically in your account.

Face Value Consideration: The debenture has a stated face value, similar to a bond. This is the amount the company “owes” you before conversion and the basis for calculating your interest payments.

How Compulsory Convertible Debentures Actually Work

Let us walk through the complete lifecycle of a CCD investment with real numbers. Understanding the actual mechanics removes confusion about how your money flows.

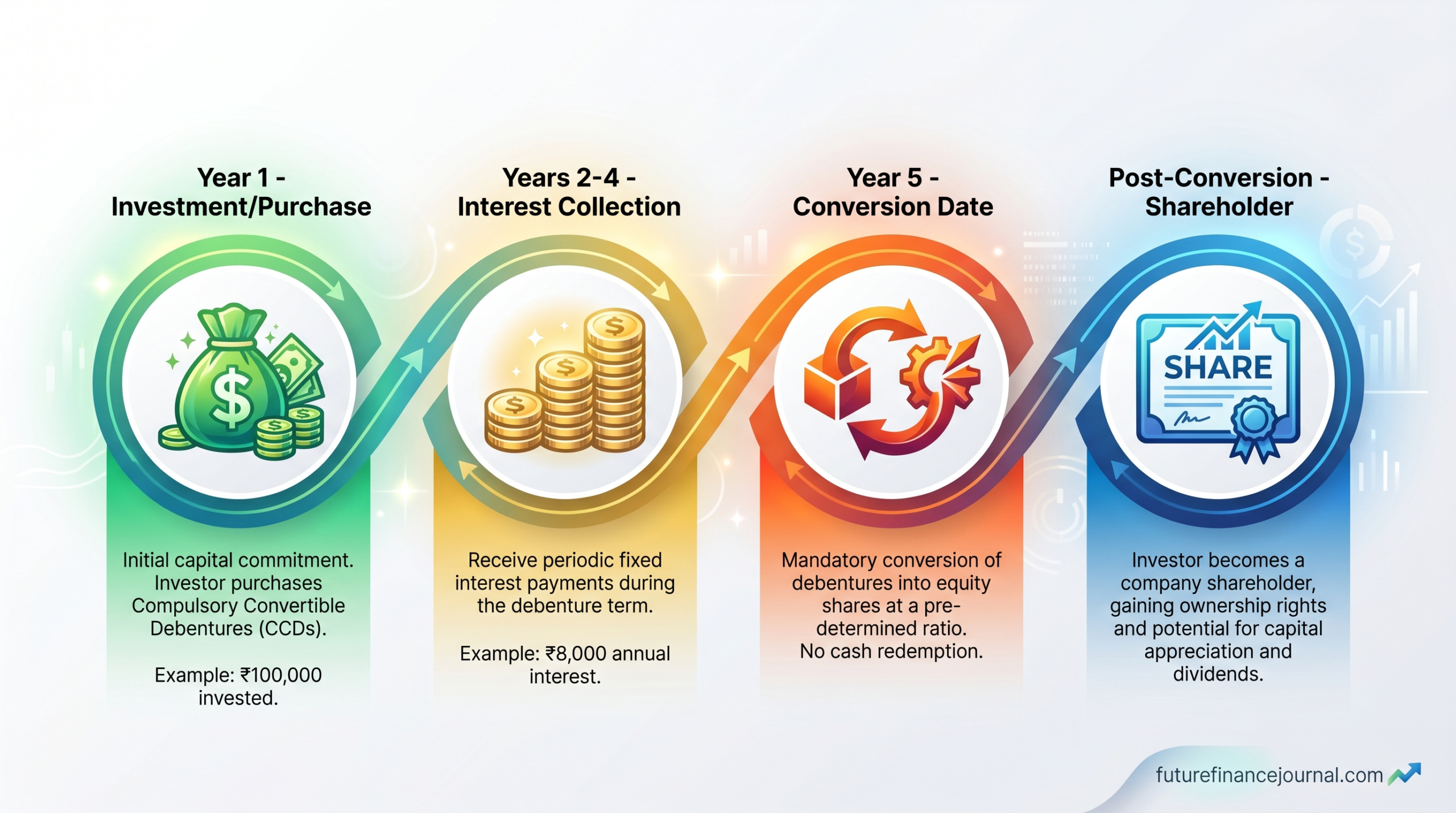

Year One: You invest 100,000 rupees in a CCD issued by a technology company. The debenture carries an 8 percent annual interest rate and will convert in five years at a ratio of 1:10 (meaning each unit converts to 10 shares). You receive your first interest payment of 8,000 rupees.

Years Two Through Four: You continue receiving 8,000 rupees annually in interest. Your money stays invested as debt. You attend shareholder meetings as a debt holder but do not yet own equity. The company’s share price may go up or down—this does not affect your interest payments.

Year Five Conversion Date: On the conversion date, your 100,000 rupee debenture automatically converts into shares. Using the 1:10 conversion ratio, you receive 10 shares. If the company’s current share price is 5,000 rupees per share, your shares are worth 50,000 rupees. If the share price climbed to 15,000 rupees, your shares are worth 150,000 rupees. If it dropped to 2,000 rupees, your shares are worth only 20,000 rupees.

Notice something important here. Your interest payments stopped giving you cash once conversion occurred. Now you own equity and your wealth depends entirely on the company’s stock performance. This is why timing and company fundamentals matter so much with CCDs.

Why Companies Issue Compulsory Convertible Debentures

Companies choose CCDs for specific strategic reasons. Understanding their perspective helps you spot which companies are in good financial health versus those desperately seeking capital.

Preserves Cash Flow: Startups and growth companies often have limited cash. Regular equity raises dilute ownership immediately. CCDs let companies access capital while pushing equity dilution several years into the future when (hopefully) they are generating profits.

Delays Dilution: Existing shareholders prefer postponing new share issuance. CCDs accomplish this goal while still raising money. Management keeps more voting power longer.

Tax Benefits: In many countries, companies deduct interest payments on debentures as expenses. This reduces taxable income. Dividend payments to shareholders are not deductible, making debentures more tax efficient.

Attracts Conservative Investors: Some investors only buy bonds or stocks, never both. CCDs appeal to bond investors by offering interest payments plus the upside potential of equity conversion later.

Maintains Control: A company issuing new equity must offer ownership stakes to outsiders. CCDs keep ownership with current shareholders until conversion actually occurs.

Growth stage companies and startups benefit most from CCDs. A ten year old software company needing fresh capital might issue CCDs converting in four years, expecting to be highly profitable by then.

Benefits for Investors Who Buy CCDs

Compulsory convertible debentures offer distinct advantages that appeal to specific investor types. These benefits explain why millions invest in CCDs despite their complexities.

Regular Income Stream: Unlike stocks, CCDs provide guaranteed interest payments. You receive these payments regardless of company performance. This creates a steady income floor before conversion.

Downside Protection: If the company struggles before conversion, you remain a debt holder with higher priority than equity shareholders. In bankruptcy, debt holders get paid before stockholders.

Upside Participation: When conversion occurs and the company flourishes, your shares participate in that growth. You get the best of both worlds: bond-like safety initially and equity-like gains later.

Lower Entry Risk: Purchasing a CCD feels safer than buying stock directly. The interest income cushions against share price drops before conversion.

Strategic Timing: Sophisticated investors use CCDs to time their equity entry. They get interest payments while waiting for the company to mature and potentially increase in value.

Consider an investor buying a CCD from a mid-size e-commerce company offering 7 percent annual interest with five year conversion. For five years, she receives regular payments and relatively stable value. After conversion, if the company grew rapidly, she now holds valuable shares without having bought at today’s higher price.

The Risks You Need to Know About

Honest evaluation requires looking at what could go wrong. Compulsory convertible debentures carry real risks that many investors underestimate.

Forced Conversion at Bad Times: You might be forced to convert exactly when the share price has dropped significantly. Bad timing means converting when shares are worth far less than your original investment. The “compulsory” part works against you here.

Shareholder Dilution: When conversion occurs, existing shareholders get diluted. Many CCDs represent substantial capital. Converting them all into equity simultaneously increases share count dramatically, reducing earnings per share for everyone.

Limited Liquidity Before Conversion: Trading CCDs is harder than trading stocks. Few buyers exist in secondary markets. If you need cash before conversion, selling might be difficult or require accepting a discount.

Company Performance Risk: If the company struggles, the share price after conversion might be worthless. You took a risk on the company as a debt holder and now you are taking that same risk as an equity holder.

Loss of Debt Protection: Once conversion happens, you lose the preferential treatment debt holders receive. You become just another shareholder, last in line during financial difficulties.

A real world example illustrates this danger. An investor bought CCDs from a ride-sharing startup in 2014, expecting conversion in 2017. By 2017, the company burned through capital and faced regulatory challenges. Forced conversion happened while share price was collapsing. The investor’s debt security evaporated.

CCDs Versus Other Convertible Securities

Several similar instruments exist in financial markets. Understanding the differences prevents confusion and helps you pick the right investment type.

Optional Convertible Debentures: These allow investors to choose whether to convert or stay as debt holders. You have flexibility that CCD investors lack. Companies prefer CCDs because they guarantee equity dilution. Investors often prefer optional convertibles for the choice.

Convertible Preference Shares: These are hybrid securities prioritizing dividend payments over common stock but not senior to debt. They offer different positioning in the company hierarchy.

Warrants: These are rights to buy shares at a set price in the future. They are pure equity instruments with no debt component or interest payments. Warrants offer leverage but no income.

Regular Bonds: Standard bonds never convert. You get predictable interest income and principal return but zero equity upside. Risk is lower but so are potential returns.

Common Stock: Direct equity ownership gives voting rights and dividend potential but no guaranteed income. Stock is purely equity risk.

The key distinction with CCDs is the mandatory nature of conversion. You give up the choice that optional convertible holders have. In exchange, companies often offer slightly higher interest rates to compensate for this loss of control.

Tax Treatment of Compulsory Convertible Debentures

Tax implications vary significantly by country and individual circumstances. This section provides general guidance applicable in most jurisdictions.

Interest Income: Interest payments on CCDs are typically taxed as ordinary income at your regular tax rate. If you earn 8,000 rupees in interest annually, that amount is taxable in that year.

Capital Gains on Conversion: When your CCD converts to shares, you may owe capital gains tax. The gain equals the difference between your share value at conversion and your original debenture cost. For detailed guidance on how conversion gains are taxed, review IRS guidance on investment income and capital gains to understand your specific tax obligations. If you bought a 100,000 rupee debenture that converted to shares worth 150,000 rupees, you have a 50,000 rupee gain.

Company Tax Benefits: The issuing company deducts interest payments as expenses, reducing corporate taxes. This is why companies prefer issuing CCDs over straight equity.

Timing Consideration: Understanding when taxable events occur helps with tax planning. Conversion creates a taxable event in the year it occurs.

Professional Advice Essential: Tax laws vary between countries and change frequently. Before investing significantly in CCDs, consult a tax professional familiar with your local rules.

How to Value and Price CCDs

Pricing a CCD requires considering multiple factors. This is more complex than valuing a simple bond or stock, but understanding the process helps you spot good deals.

Underlying Share Price: The current stock price matters because it indicates what you will own after conversion. If shares currently trade at 5,000 rupees and your conversion ratio gives you 10 shares, the conversion value today is 50,000 rupees.

Interest Rate Offered: Higher interest rates make CCDs more attractive. If one CCD pays 6 percent and another pays 10 percent, the higher rate offers better income while waiting for conversion.

Time to Conversion: Longer wait times mean more interest payments but extended uncertainty. A 3-year conversion timeframe involves different risk than a 10-year horizon.

Company Financial Health: Strong companies with growing revenue make better CCDs than struggling firms. Examine balance sheets, debt levels, and cash flow before investing.

Market Conditions: Rising interest rates make new CCDs more attractive compared to older ones issued at lower rates. Economic downturns increase company risk.

Fair Value Calculation: A simple approach values a CCD as the present value of future interest payments plus the expected share value at conversion. If you expect 8,000 rupees annual interest for three years and shares worth 100,000 rupees at conversion, you can calculate a fair purchase price.

Sophisticated investors use option pricing models for more precise valuations. The convertible feature functions like an option on the stock. But for most investors, understanding the basic factors above suffices.

The Conversion Process Explained

When the conversion date arrives, several things happen automatically. Understanding this process removes surprises and helps you plan ahead.

Automatic Conversion: On the specified date, your debenture account shows zero balance. Your share account simultaneously shows your new shares. No action is required on your part.

Share Allotment Timeline: Most companies allot shares within 2-3 business days of conversion. You can typically see the shares in your demat account shortly after. Some delays happen occasionally due to administrative processes.

No Conversion Fee: Companies do not charge fees for converting debentures to shares. The conversion happens at no additional cost to you.

Certificate Updates: Your investment statement updates to show equity shares instead of debentures. Your demat account receives the new shares.

Dividend Eligibility: After conversion, you become eligible for dividends on the new shares. You get voting rights like any shareholder.

Tax Documentation: Your company will send documentation showing the conversion details needed for tax purposes. Keep these records for tax filing.

The conversion process is straightforward and happens behind the scenes. You do not need to submit forms or sign documents unless your company requires specific authorization upfront.

Real World Examples of CCD Usage

Several major companies have successfully used compulsory convertible debentures. These examples show different scenarios and outcomes.

Example 1: Growth Stage Technology Company

A mid-sized software company issued 50 crore rupees in CCDs in 2018 at 7 percent interest, converting in 2023. The company used the capital to expand its engineering team and open new offices. By 2023, revenues had tripled and profits grew substantially. The share price had increased 180 percent. Investors who converted received shares worth significantly more than their original investment plus five years of interest income.

Example 2: Struggling Manufacturing Firm

A textile company issued CCDs in 2019 needing cash during sector downturn. The company planned to modernize facilities. Instead, the sector continued struggling and the company faced margin pressure. By the 2023 conversion date, share price had fallen 45 percent. Investors converted into shares worth far less than they invested. They lost money despite receiving interest income during the holding period.

Example 3: Successful Startup Conversion

An online payments startup issued 25 crore rupees in CCDs in 2019 at 8 percent interest, converting in 2024. The company captured massive market growth as digital payments expanded. By conversion time, revenue had grown 400 percent. The share price jumped 320 percent. Investors received shares that had become extremely valuable, far exceeding their initial investment.

These examples highlight that CCD outcomes depend heavily on company performance. Good companies with strong management create excellent returns. Weak companies or bad timing create losses.

Regulatory Framework and Legal Aspects

Compulsory convertible debentures operate within specific regulatory frameworks designed to protect investors and maintain market integrity.

SEBI Regulations: In India, the Securities and Exchange Board of India (SEBI) governs CCD issuance through detailed rules on disclosure, pricing, and investor protection. For comprehensive information on debenture regulations, visit SEBI official guidelines on debenture issuance to understand the exact requirements that companies and investors must follow.Companies must follow these rules precisely.

Disclosure Requirements: Companies must clearly state all CCD terms including conversion ratio, conversion date, interest rate, and redemption features. Misleading disclosures face severe penalties.

Investor Protection: Regulations protect minority investors from unfair treatment. Anti-dilution clauses sometimes protect CCD holders if the company takes certain actions before conversion.

Rights and Obligations: Legal documents specify exactly what rights you have and what obligations the company has. Reading these documents matters before investing.

Insolvency Considerations: During company insolvency, regulations determine where CCD holders rank relative to other creditors and shareholders. Rank is typically between regular debt and equity.

Different Rules by Country: Other countries have different regulatory frameworks. CCDs in United States markets follow SEC rules. European CCDs follow different regulations. Australian CCDs have their own framework.

Who Should Consider Investing in CCDs?

Compulsory convertible debentures work well for certain investors but not others. Identifying if you fit the right profile matters.

Conservative Growth Investors: People wanting regular income but also seeking equity upside benefit most from CCDs. You get bond-like payments plus eventual stock ownership.

Patient Long-Term Investors: The multi-year holding period before conversion suits investors who can wait 3-7 years without needing capital. Short-term traders should avoid CCDs.

Believers in Company Growth: If you genuinely believe a company will flourish before conversion, CCDs let you participate while collecting interest. Skeptics should avoid forced equity exposure.

Moderate Risk Tolerance: CCDs suit investors comfortable with moderate risk. They are riskier than bonds but safer than stocks until conversion.

Diversified Portfolio Builders: Adding a few CCDs to a diversified portfolio adds variety. They serve as a bridge between pure debt and pure equity positions.

Wealth Accumulation Phase: Younger investors or those still in earning years can absorb conversion risks better than retirees needing stable income.

Common Mistakes to Avoid with CCDs

Knowing what goes wrong helps you make better investment decisions.

Ignoring Conversion Terms: Many investors buy CCDs without fully understanding the conversion ratio, date, or terms. Read every detail. Ask questions until everything is clear.

Overlooking Company Fundamentals: Buying a CCD without analyzing company finances is dangerous. Examine balance sheets, debt levels, cash flow, and competitive position before investing.

Misunderstanding Forced Conversion: Expecting flexibility or optional conversion with a CCD is a mistake. The mandatory nature means conversion happens whether you want it or not.

Not Calculating Dilution Impact: Every new share issued dilutes existing shares. Calculate how CCD conversion affects earnings per share and your ownership percentage.

Expecting Liquidity That Does Not Exist: Many CCDs trade rarely in secondary markets. If you might need cash before conversion, avoid CCDs. Stock and bonds are far more liquid.

Chasing High Interest Rates: A CCD offering 15 percent interest when others pay 7 percent signals hidden risk. Higher rates compensate for higher risk.

How CCDs Fit Into Your Investment Portfolio

Strategic allocation of CCDs within your broader portfolio matters. You should not load up excessively on any single security type.

Typical Allocation: Conservative portfolios might hold CCDs as 5-10 percent of total investments. Growth-focused portfolios might hold 0-5 percent. Nobody needs massive CCD exposure.

Role in Diversification: CCDs provide different risk-return characteristics than pure debt or pure equity. They reduce portfolio volatility while capturing equity upside.

Balancing Risk: Use CCDs to moderate overall portfolio risk. If you already own significant equity, adding CCDs adds more equity risk through conversion. If you own mostly bonds, CCDs shift you toward equity exposure.

Sector Consideration: Diversify your CCDs across different sectors and companies. Owning three CCDs from three different technology companies creates concentration risk.

Rebalancing: As conversion approaches, plan how the new shares fit your portfolio. You may need to rebalance to maintain your target allocation.

Final Thoughts and Next Steps

Compulsory convertible debentures are legitimate financial instruments serving specific purposes for both companies and investors. They are not mysterious or overly complex once you understand the basics.

The key insight is simple: you are lending money to a company for regular interest payments, but you automatically become a shareholder after a set period. This hybrid nature works well for patient investors believing in company growth but wanting income along the way.

Before investing in any CCD, evaluate the issuing company carefully. Strong companies with good management create excellent CCD opportunities. Weak companies or poor timing create losses. Interest payments provide some cushion, but conversion risk remains substantial.

Start by reading the CCD prospectus completely. Understand every term. Ask questions until confusion disappears. Consult with financial advisors about whether CCDs match your goals and risk tolerance.

Consider starting with one or two CCDs from established companies you trust. Learn how the conversion process works. Build understanding before making larger commitments.

Compulsory convertible debentures deserve consideration as part of a diversified investment approach, but they are not suitable for everyone. Evaluate honestly whether your investment goals, risk tolerance, and time horizon align with CCD characteristics. Make decisions based on facts rather than chasing yields or hoping for quick profits.

Your investment journey improves when you understand what you own and why you own it. CCDs are no different. Take time to educate yourself, ask questions, and make deliberate choices that support your long-term financial success.